Table of Contents >> Show >> Hide

- The Simple Definition of Amortization

- How Amortization Works for Loans

- A Clear Example of Amortization

- What an Amortization Schedule Shows

- Why Amortization Matters in Real Life

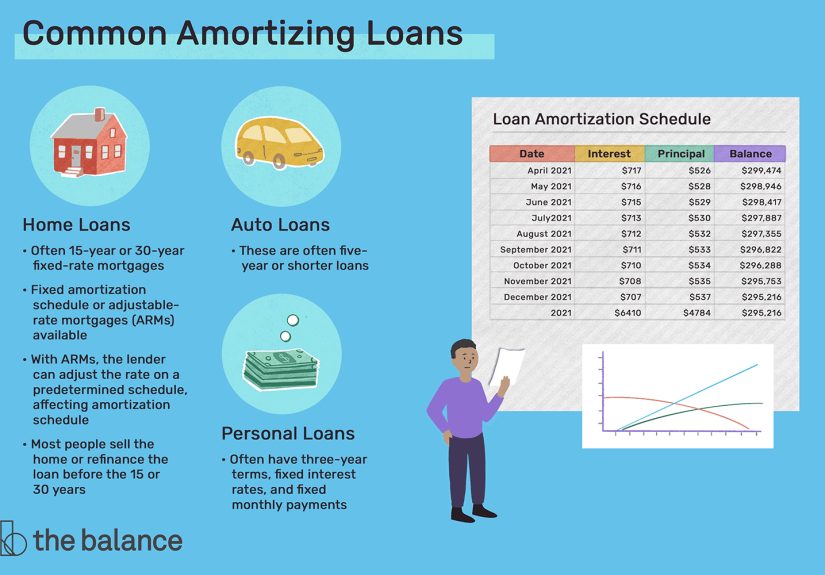

- Which Loans Are Amortizing Loans?

- When a Loan Does Not Amortize Normally

- Amortization in Accounting

- Amortization vs. Depreciation

- Common Misunderstandings About Amortization

- How to Use Amortization to Make Better Financial Decisions

- Real-World Experiences With Amortization

- Conclusion

- SEO Tags

Amortization sounds like one of those financial words invented to make regular people close their laptops and go “absolutely not.” But the idea is much simpler than the word. In everyday lending, amortization is the process of paying off debt through scheduled payments over time. In accounting, amortization is the gradual expensing of certain intangible assets, such as patents, licenses, or other finite-lived business rights. Same word, two related meanings, one shared goal: spreading cost over time instead of swallowing it all at once.

If you have ever looked at a mortgage statement and wondered why your monthly payment feels heroic while the balance seems to shrink like a sleepy snail, you have already met amortization. If you have ever heard an accountant talk about intangible assets and quietly decided to check your email instead, you have also brushed against it. This guide breaks it all down in plain English, with examples, real-world context, and enough detail to make the concept useful instead of merely decorative.

The Simple Definition of Amortization

At its most basic, amortization means spreading something out over time.

For loans, amortization is the structured repayment of borrowed money through regular installments. Each payment usually includes two parts: principal and interest. Principal is the amount you borrowed. Interest is the price of borrowing it. Over time, the loan balance falls until it reaches zero, assuming the loan is fully amortizing and you make payments as agreed.

For accounting, amortization means gradually writing off the cost of an intangible asset over its useful life. Instead of treating the cost as one giant expense in year one, the business recognizes portions of it across several years.

So yes, amortization wears two outfits. One outfit shows up in consumer finance. The other lives in accounting. Both revolve around timing, allocation, and the wonderfully adult activity of not doing everything all at once.

How Amortization Works for Loans

Every Payment Has a Job

When you make a payment on an amortizing loan, the money is not dumped randomly into a financial blender. It is divided according to the loan terms. Part goes to interest. Part goes to principal. In the early stage of the loan, more of the payment usually goes toward interest. Later, more goes toward principal.

This is why new borrowers sometimes feel personally betrayed by their first year of statements. The payment amount may stay the same, but the mix inside the payment changes over time.

Why Interest Takes the First Slice

Interest is generally calculated on the outstanding balance. Early in the loan, that balance is still large, so the interest portion is larger too. As you gradually pay down the principal, the balance shrinks, and less interest accrues. That frees up more of each later payment to attack the principal.

That shifting balance between interest and principal is the heart of loan amortization. Same payment. Different internal proportions.

The Amortization Formula

For a fixed-rate loan, lenders use a standard formula to calculate a level payment that will fully pay off the balance by the end of the term. The common formula looks like this:

Payment = P × r / (1 - (1 + r)^-n)

In that formula:

- P = principal

- r = periodic interest rate

- n = total number of payments

You do not need to memorize it unless that is your idea of a good weekend. What matters is what the formula accomplishes: it creates a payment amount that covers interest and steadily reduces the balance to zero on schedule.

A Clear Example of Amortization

Let’s say you borrow $300,000 for a 30-year fixed mortgage at 6.5% interest. Using the standard loan-payment formula, your monthly principal-and-interest payment would be about $1,896.20.

That does not mean you are paying $1,896.20 straight into the loan balance every month. In the early months, a large share goes to interest because the outstanding balance is still high. Over time, the interest portion falls and the principal portion rises.

Now imagine the same borrower comparing loan terms at 5.5%:

- A 30-year loan would have a payment of about $1,703.37 per month.

- A 15-year loan would have a payment of about $2,451.25 per month.

The 15-year option costs more each month, but it dramatically cuts total interest over the life of the loan. That is one of the most important practical lessons in amortization: a longer term often lowers the payment, but it usually increases the total borrowing cost.

In other words, amortization helps answer a grown-up question with very real consequences: do you want lower monthly pain, or less total pain?

What an Amortization Schedule Shows

An amortization schedule is a table that maps the life of your loan payment by payment. It usually includes:

- Payment number

- Payment date

- Total payment amount

- Interest paid

- Principal paid

- Remaining balance

This schedule is more than just a bureaucratic spreadsheet with trust issues. It is a decision-making tool. It lets you see how slowly or quickly you are building equity, how much interest you are paying, and how extra payments could change the life of the loan.

For example, if you make an extra principal payment each month, even a modest one, you can shorten the loan term and reduce total interest. The schedule makes that visible. It turns vague financial optimism into math you can actually use.

Why Amortization Matters in Real Life

It Affects Affordability

Two loans with the same balance can feel very different because amortization changes the payment structure. A longer loan term usually lowers the monthly payment, which can help cash flow. But that convenience often comes with more interest paid over time.

It Affects Equity Building

On amortizing mortgages, you typically build equity slowly at first and faster later, unless home values rise independently. This matters if you plan to move, refinance, or sell within a few years.

It Affects Refinance Decisions

Refinancing can lower the monthly payment, but it can also restart the amortization clock. That means you may go back to a payment structure that tilts heavily toward interest in the early years. A refinance can still make sense, but only if you understand what is happening under the hood.

It Affects Extra Payments

When extra money goes straight to principal, the future interest bill can shrink because interest is calculated on a lower balance. That is why borrowers who make targeted extra principal payments often save more than they expect.

Which Loans Are Amortizing Loans?

Many common installment loans use amortization, including:

- Fixed-rate mortgages

- Auto loans

- Personal loans

- Student loans with fixed repayment structures

- Some small business term loans

Not every debt works this way, though. Credit cards usually do not follow a classic amortization schedule because the balance can revolve and the required payment can vary. Some mortgages also have unusual structures, such as interest-only periods or balloon payments.

When a Loan Does Not Amortize Normally

Interest-Only Loans

During an interest-only period, the borrower pays only interest and does not reduce principal. That can lower the payment temporarily, but it does not steadily retire the balance.

Balloon Loans

A balloon loan may have smaller payments for a while, followed by a large final payment. It is not the same as a fully amortizing loan, which is designed to reach a zero balance by the end of the term.

Negative Amortization

Negative amortization is the villain in this story. It happens when the payment is not enough to cover the interest due. Instead of going down, the balance grows. That is the financial equivalent of running on a treadmill while someone quietly increases the incline.

This is why borrowers should never judge a loan only by the monthly payment. Payment size matters, but payment structure matters just as much.

Amortization in Accounting

Now for the accounting side of the word.

In business accounting, amortization is the systematic allocation of the cost of an intangible asset over its useful life. Intangible assets are nonphysical assets that still have economic value. Think patents, trademarks, customer relationships, franchise rights, licenses, and certain software-related rights.

If a company buys a patent with a useful life of 10 years, it may amortize that cost over 10 years instead of recording the full amount as an immediate expense. This helps match the expense to the period in which the asset helps generate revenue.

Here is the key distinction:

- Finite-lived intangible assets are typically amortized over their useful lives.

- Indefinite-lived intangible assets are generally not amortized while they remain indefinite-lived. Instead, they are evaluated for impairment.

This is where people often get tangled up, because tax rules and financial accounting rules are not always identical twins. For example, certain acquired intangible assets may be amortized under tax law using a prescribed schedule, while financial reporting may apply different useful-life logic under GAAP.

Amortization vs. Depreciation

These two terms are cousins, not clones.

Amortization usually applies to intangible assets or to loan repayment schedules.

Depreciation applies to tangible assets, such as buildings, machinery, furniture, or vehicles used in business.

If a company buys delivery trucks, it generally depreciates them. If it acquires a finite-lived patent or license, it generally amortizes that cost. If you borrow money to buy either one, your loan may also amortize. Yes, finance loves reusing words just to keep everyone alert.

Common Misunderstandings About Amortization

- “A fixed payment means I pay the same amount of principal every month.”

Not usually. On a standard amortizing loan, the total payment may stay the same, but the split between interest and principal changes. - “A lower monthly payment always means a better deal.”

Not necessarily. A lower payment may come from a longer term, which often means more interest paid overall. - “If I refinance and my payment drops, I automatically save money.”

Maybe, maybe not. You need to compare total costs, time in the home, fees, and whether the new schedule resets the interest-heavy early years. - “Amortization is only a mortgage thing.”

Nope. It appears in auto loans, personal loans, student loans, business loans, and accounting for intangible assets.

How to Use Amortization to Make Better Financial Decisions

If you want amortization to work for you instead of lurking in the fine print, focus on these moves:

- Review the amortization schedule before you borrow. Do not stop at the monthly payment.

- Compare loan terms side by side. The cheaper monthly option may be much more expensive in total.

- Ask how extra payments are applied. Make sure extra money goes to principal if that is your goal.

- Watch out for interest-only and negative-amortization features. Small payments can hide large future problems.

- For business assets, understand the accounting treatment. The useful life of an asset can shape reported earnings and tax treatment.

Amortization is not just an accounting concept or a lender’s spreadsheet hobby. It is one of the clearest tools for understanding how cost, time, and borrowing interact.

Real-World Experiences With Amortization

To make this concept less abstract, here are common experiences people have when amortization leaves the classroom and enters real life wearing work boots.

The first-time homebuyer experience: A buyer closes on a house, proudly makes six on-time mortgage payments, then checks the balance expecting dramatic progress. Instead, the principal has moved, but not by much. Panic briefly enters the chat. Then comes the realization: this is how mortgage amortization works. In the early years, a bigger share of the payment goes to interest. It does not mean the loan is broken. It means the borrower has finally seen the math behind homeownership.

The car-loan wake-up call: A borrower picks the longest term available because the payment looks easier to manage. Months later, they realize the car is aging faster than the loan balance is shrinking. That does not mean the loan was wrong, but it does highlight a core truth: amortization affects flexibility. A lower payment can help cash flow, but it can also keep the borrower underwater longer if the vehicle depreciates quickly.

The extra-payment victory: Another borrower decides to add just a little extra to the principal each month. Not enough to star in a motivational finance documentary, just enough to matter. Over time, the schedule changes. Interest costs fall. The loan ends earlier than expected. This is one of the most satisfying things about amortization: small, consistent actions can create outsized long-term results.

The refinance confusion: Someone refinances to lower a monthly payment and feels relieved. Good move, maybe. But then they discover they restarted the loan over a longer term. Their payment is lower, yet the total interest may end up higher unless they keep paying aggressively or stay in the loan long enough for the lower rate to offset the reset. This is why understanding amortization can save you from celebrating too early with grocery-store cake.

The small business accounting moment: A business owner acquires a customer list, license, or patent-related right and expects the whole cost to hit the books instantly. Instead, the cost is spread over years. At first, this feels annoying. Then it starts to make sense. The asset is expected to help generate value over time, so the expense is recognized over time too. That is amortization doing its quiet, orderly thing in the accounting world.

The emotionally useful lesson: Many people assume financial progress should feel dramatic every month. Amortization teaches the opposite. Progress is often front-loaded with discipline and back-loaded with visible results. Early on, change can look small. Later, the same structure begins to work in your favor faster. That lesson applies to loans, budgeting, and honestly, half of adulthood.

So if amortization ever feels dry, remember this: behind the spreadsheets are real decisions about homes, cars, businesses, cash flow, and long-term tradeoffs. Once you understand it, you are no longer just making payments. You are reading the story your money is telling over time.

Conclusion

Amortization is the process of spreading repayment or cost over time. In lending, it explains how fixed payments gradually pay off principal and interest. In accounting, it explains how certain intangible assets are expensed across their useful lives. The concept may sound technical, but its practical value is huge. It helps borrowers compare loans, understand equity growth, evaluate refinancing, and see the real cost of a debt beyond the monthly payment. It also helps businesses match costs to the periods that benefit from those assets.

Once you understand amortization, a payment schedule stops looking like financial wallpaper and starts looking like useful information. And that is a lovely upgrade for one word that usually arrives looking suspiciously like homework.