Table of Contents >> Show >> Hide

- What Is a Bear Market, Really?

- Nominal vs. Real Returns: The Bear You Don’t See

- Why Bonds Can Suffer the Deepest “Invisible” Bear Markets

- Shallow Risk vs. Deep Risk

- Sequence-of-Returns Risk: When a Bear Market Shows Up at the Worst Time

- What History Teaches Us About Bear Markets

- How to Protect Yourself from the Worst Kind of Bear Market

- Putting It All Together: A Common-Sense Checklist

- Real-World Experiences: What the “Worst Bear Market” Feels Like

- Conclusion: Use Common Sense to Fight the Invisible Bear

If you’ve been investing for more than about five minutes, you’ve probably heard the classic definition of a bear market: stock prices fall 20% or more, everyone panics, financial TV goes full drama mode, and your phone lights up with “Should I sell?” messages.

But that’s not actually the worst kind of bear market.

The worst bear market is sneakier. It doesn’t always show up as a scary red number on your statement. Instead, it quietly eats away at what your money can buy. On paper, your account balance might look fineeven higher than last year. But when you go to the grocery store, fill up the car, or book a vacation, you realize your “gains” have gone missing in real life.

That’s the wealth-destroying combo of inflation and poor real returnsthe kind of long, grinding bear market that inspired Ben Carlson’s famous post “The Worst Kind of Bear Market” on his blog, A Wealth of Common Sense. In this article, we’ll unpack what that actually means, why it hits bond investors especially hard, and how you can protect yourself with a little bit of, well, common sense.

What Is a Bear Market, Really?

Let’s start with the basics. Most financial pros define a bear market as a decline of 20% or more in a broad market index like the S&P 500 from a recent high. That’s the version you hear about in headlinesstocks plunge, investors panic, and pundits dust off their “Is this 1929 again?” segments.

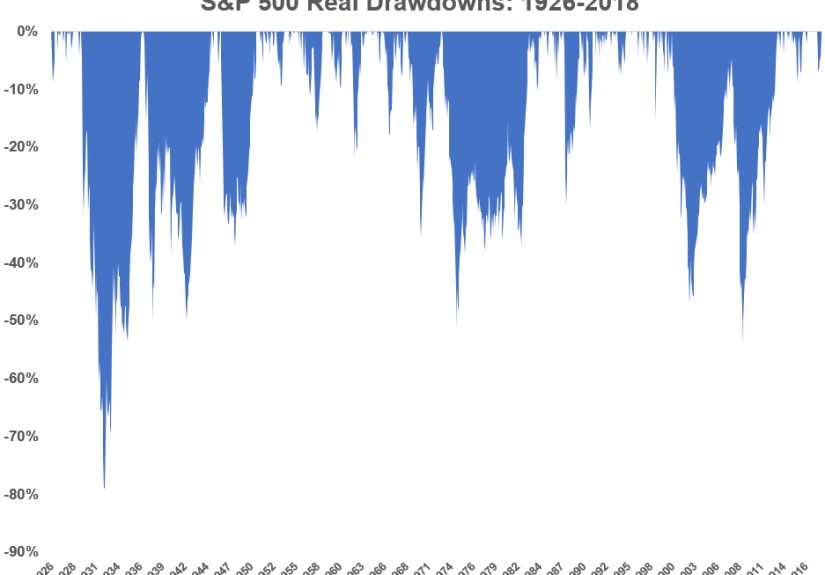

Historically, bear markets are normal. From 1928 onward, U.S. stocks have seen more than 20 distinct bear markets. According to several long-run studies, the typical bear market lasts around 9–15 months, with recoveries taking another couple of years on average. They’re painful, but they usually resolve in a timeframe that, while uncomfortable, doesn’t permanently derail long-term investors who stay the course.

That’s the “headline bear market” most people worry about: sharp price declines over a relatively short period. But there’s another layer that matters even more: what happens after inflation.

Nominal vs. Real Returns: The Bear You Don’t See

Your brokerage statement is quoted in nominal dollarsthe raw number of dollars in your account. Unfortunately, real life runs on real dollarsthose same dollars adjusted for inflation. If your portfolio returns 5%, but inflation is 7%, your “gain” is actually a loss in disguise. Your money buys less, even though the line on your chart is going up.

That’s the key insight from Carlson’s analysis. Using long-term data, he compared the inflation-adjusted (real) drawdowns for U.S. stocks and U.S. bonds going back to the 1920s. The surprise? Stocks have had some vicious crashes, but their longest real bear market was roughly 13 years (2000–2013) before fully recovering after inflation. Bonds, on the other hand, experienced a real bear market that lasted about five decades.

Let that sink in: five-year U.S. Treasuries and long-term Treasuries went through a real drawdown from around 1940 to the mid-1980s where investors lost 40–70% of their purchasing power, even though nominal returns looked “pretty decent.” On paper, bond investors were earning 4–5% a year. In real life, inflation was quietly torching their standard of living.

That’s the worst kind of bear market: the one you don’t notice until it’s too late.

Why Bonds Can Suffer the Deepest “Invisible” Bear Markets

When people think “risky,” they usually think “stocks.” Stocks are volatile. They crash. They make scary headlines. Bonds, by comparison, seem calm and boring. But boring doesn’t necessarily mean safe in all environments.

Here’s the crucial distinction:

- Stocks are most vulnerable to sudden crashes (shallow but dramatic drawdowns).

- Bonds are most vulnerable to prolonged periods of high inflation (slow, grinding real losses).

In the 1940–1981 period, interest rates drifted higher for decades as inflation picked up, especially in the 1970s. Existing bondholders got hit from both sides: rising rates pushed down bond prices, and high inflation eroded the purchasing power of the interest they were earning. Even though their statements showed positive nominal returns year after year, their real wealth was shrinking.

This is why some financial historians and practitioners call this a “death by a thousand cuts” bear market. There’s no single dramatic crash you can point to. Instead, you wake up one day and realize the same “safe” bonds that looked so steady have quietly made you poorer in real terms.

Shallow Risk vs. Deep Risk

To make sense of these different dangers, author and financial thinker William Bernstein introduced a helpful framework: shallow risk vs. deep risk.

- Shallow risk is a temporary decline that recovers in a few years. It’s scary, but if you don’t sell at the wrong time, you eventually recover.

- Deep risk is a long-term or permanent loss of purchasing power. It may be caused by inflation, confiscation, war, or severe financial repression.

Most stock bear markets are shallow risks: brutal but relatively short-lived. The long, inflation-fueled bond bear market of the mid-20th century is a classic example of deep risk. Nominally, investors were “fine.” In real terms, many lost half or more of their purchasing power.

The lesson is uncomfortable but important: if your portfolio is built only around avoiding volatility, you might be trading short-term emotional comfort for long-term financial damage.

Sequence-of-Returns Risk: When a Bear Market Shows Up at the Worst Time

There’s another nasty cousin to the worst kind of bear market: sequence-of-returns risk. This is the risk that you experience poor or negative returns early in retirementright when you’re starting to draw down your savings.

Two retirees can earn the same average return over 30 years, but if one gets the bad years at the beginning and the other gets them at the end, their outcomes can be radically different. Early losses combined with withdrawals can permanently damage a portfolio, especially if inflation is also high.

Retiring into a long, inflationary bear marketwhether in stocks, bonds, or bothcan feel like being hit from every direction: rising prices, weak real returns, and the need to withdraw money to live on. That’s why planners spend so much time modeling different sequences of returns and stress-testing portfolios against prolonged bear markets.

What History Teaches Us About Bear Markets

If you zoom out over the past century, you’ll find all kinds of bear markets:

- The Great Depression crash (1929–1932)

- The post-World War II and 1970s inflationary period

- The dot-com bust (2000–2002)

- The Global Financial Crisis (2007–2009)

- The COVID-19 crash in 2020

Each one had different causesspeculation, banking crises, recessions, pandemics, policy errors. But across many of these events, especially the inflationary episodes, one pattern shows up: investors who focused only on nominal returns and short-term comfort often fared worse in real terms than those who accepted some volatility in exchange for long-term growth.

In other words, trying too hard to avoid the “visible” bear market can sometimes lead you straight into the invisible one.

How to Protect Yourself from the Worst Kind of Bear Market

So what does common sense suggest if the worst bear market is the one that quietly erodes your purchasing power?

1. Think in Real Terms, Not Just Nominal Dollars

Make it a habit to mentally adjust for inflation. If your portfolio is earning 4% and inflation is 3%, your real gain is about 1%. If inflation is 5%, that same 4% return is actually a loss.

Whenever you evaluate performance, ask, “How did I do relative to inflation?” That simple question can keep you from getting too comfortable with low-yield, long-duration fixed income when inflation risk is rising.

2. Own Assets with Long-Term Growth Potential

Over long periods, stocks have dramatically outpaced inflation and bonds in real terms. From the 1920s onward, $1 invested in U.S. stocks and held through the ups and downs grew to hundreds of dollars in real purchasing power, while the same dollar in bonds grew only to single-digit real amounts.

That doesn’t mean you should be 100% in stocks at all times. It does mean that if your goal is to preserve and grow purchasing power over decades, you generally need some exposure to assets that can grow faster than inflationequities, real estate, and certain types of inflation-linked bonds.

3. Diversify Across “Shallow” and “Deep” Risks

No single asset class protects you from everything. A reasonable portfolio accepts that some pieces are better at handling shallow risk (temporary crashes), while others help with deep risk (long-term inflation and structural changes).

- Cash and short-term bonds can help with near-term spending and reduce the need to sell volatile assets at bad times.

- Stocks and real estate can help keep up with or outpace inflation over the long run.

- Inflation-linked bonds (like TIPS in the U.S.) can offer explicit inflation protection for part of your portfolio.

The mix depends on your time horizon, risk tolerance, and cash-flow needsbut thinking explicitly about both shallow and deep risk is the starting point.

4. Match Your Portfolio to Your Time Horizon

One of Bernstein’s most practical points is that money for near-term goals should be invested differently from money for long-term goals. Capital you’ll need in the next 3–5 years shouldn’t be riding out 50% stock market drawdowns. Money you won’t touch for 20–30 years shouldn’t sit entirely in assets that are vulnerable to decades of inflation.

This “time-bucketing” approach helps you avoid panic-selling during shallow-risk events and protects long-term assets from deep-risk erosion.

5. Don’t Let Fear of Volatility Push You into Long-Term Losses

Many investors are volatility-averse. That’s human. Watching your portfolio drop 20–30% in real time is emotionally brutal. The temptation is to flee to “safe” long-term bonds or cash as soon as things get rough.

The problem is that if you lock in very low yields during an inflationary period, you may be walking straight into the worst kind of bear marketslow, persistent loss of purchasing power. Nominal stability can be a trap.

Common sense doesn’t mean being fearless. It means recognizing that short-term discomfort can sometimes be the price of long-term security.

Putting It All Together: A Common-Sense Checklist

When you hear “bear market,” don’t just think about falling prices. Think about your real-life standard of living. A practical checklist might look like this:

- Am I tracking my returns relative to inflation, not just in nominal dollars?

- Do I own assets that can grow faster than inflation over decades?

- Is my bond exposure balanced between providing stability and avoiding long-term inflation damage?

- Have I thought about sequence-of-returns risk for retirement or upcoming withdrawals?

- Is my portfolio aligned with my actual time horizons, not just my risk tolerance questionnaire?

If you can answer “yes” to most of those questions, you’re far better prepared for both the visible and invisible bear markets.

Real-World Experiences: What the “Worst Bear Market” Feels Like

It’s one thing to talk about real returns and inflation. It’s another to feel it in everyday life. To make this more concrete, let’s walk through a few experience-based scenarios that capture what the worst kind of bear market actually looks like for real people.

The Cautious Saver Who Stayed “Safe”

Imagine a diligent saver named Linda. She hates volatility, so over the years she avoids stocks almost entirely. Instead, she piles her money into long-term government bonds that seem safe and stable. For decades, her statements show steady nominal returns of 4–5% a year. No big crashes. No scary volatility. It feels like she’s winning.

Fast-forward 30 years. Prices of groceries, healthcare, and housing have quietly climbed higher and higher. The monthly interest check from Linda’s bond portfolio hasn’t kept up. The account balance looks healthy on paper, but when she calculates how many months of living expenses it really covers, she realizes her “safe” portfolio has lost a big chunk of its purchasing power to inflation.

Linda never lived through a big headline crash. Instead, she lived through the worst bear marketthe one that doesn’t show up obviously on a chart but shows up painfully in her day-to-day budget.

The New Retiree Who Hit a Double Whammy

Now consider James, who retires right as markets enter a prolonged slump. Stock returns are weak for several years, inflation spikes, and headlines are full of “Is this the next big crash?” pieces. His portfolio is diversified, but he still needs to withdraw a fixed amount each year to cover living expenses.

Because markets are down early in his retirement, every dollar he withdraws sells more shares at lower prices. Combine that with rising costs at the grocery store and gas pump, and James feels squeezed from both ends. This is sequence-of-returns risk in real time: poor early returns plus withdrawals plus inflation.

What James experiences feels like a never-ending bear market. Even small day-to-day price increases feel enormous because his portfolio doesn’t seem to catch a break. Without a clear plansuch as flexible withdrawal rules or a cash bufferhe might be tempted to abandon his long-term allocation at exactly the wrong time.

The Long-Term Investor Who Embraced Volatility (Within Reason)

Finally, picture Maya. She doesn’t enjoy volatility either (no one truly does), but she understands the trade-off between shallow and deep risk. She keeps enough cash and short-term bonds to cover several years of living expenses and emergencies. The rest of her portfolio is spread across global stocks, some real estate exposure, and a slice of inflation-protected bonds.

During sharp stock market crashes, Maya’s portfolio takes a visible hit. Her net worth drops on paper. But she doesn’t need to sell stocks to pay her bills because that cash and short-term bond bucket gives her breathing room. Over time, as markets recover, her growth assets help her keep up with, and eventually outpace, inflation.

Maya still experiences bear marketsbut mostly the headline kind, the shallow risks that recover. Because she’s thought carefully about deep risk, she’s less vulnerable to the slow, invisible erosion that devastated bond-heavy investors in past inflationary periods.

The Emotional Side of Invisible Bear Markets

What often makes the worst kind of bear market so dangerous is that it doesn’t feel urgent. A 30% market crash grabs your attention. A 2–3% yearly erosion of real purchasing power does not. It’s easy to rationalize: “I’m not losing money; my account balance is going up.”

But over 10, 20, or 30 years, that slow drip can be more damaging than a short, sharp crash. The emotional trap is that people tend to react strongly to visible, immediate losses and ignore slow, compounding ones. Having a “wealth of common sense” means training yourself to pay attention to both.

Talking through these scenarios with a financial professional, or even just modeling them in a simple spreadsheet, can be eye-opening. Seeing how different mixes of stocks, bonds, cash, and inflation-linked assets behave in various historical periods can help you choose a strategy you can actually stick withone that respects both your need for sleep today and your need for sustenance in the future.

At the end of the day, the worst kind of bear market isn’t just about markets at all. It’s about life: what your money can do for you, how secure you feel, and whether your future self will look back and say, “I protected my purchasing power,” instead of “I played it safe and quietly fell behind.”

Conclusion: Use Common Sense to Fight the Invisible Bear

The classic bear marketthe 20%+ drop that dominates headlinesis scary but visible. It’s the monster in the movie that jumps out at you. The worst kind of bear market is subtler: a long period where inflation quietly outpaces your returns, leaving your account looking fine while your lifestyle shrinks.

A wealth of common sense says you need to watch both. Think in real terms, not just nominal. Own at least some assets that can outrun inflation. Balance shallow and deep risks in your portfolio. And match your investments to your time horizons so you’re not forced into bad decisions when markets get rough.

Markets will always have new bear phases, new crises, and new scary headlines. But the core principles don’t change: focus on purchasing power, stay diversified, respect both kinds of risk, and let common sensenot feardrive your decisions.