Table of Contents >> Show >> Hide

- What Is a Melt-Up, Exactly?

- Why the Melt-Up Thesis Is Back on the Table

- The Bullish Case: Why a Melt-Up Could Keep Going

- The Bearish Case: Why the Melt-Up Story Can Turn Messy

- How Melt-Ups Usually End

- What to Watch If You Are Revisiting the Melt-Up Scenario

- The Real Takeaway

- Experiences From the Front Row of a Melt-Up

Every few years, the market starts behaving like it just discovered cold brew, confidence, and a questionable amount of leverage all at once. Prices rise fast. Skeptics keep waiting for gravity. Latecomers panic-buy because missing the rally suddenly feels more painful than overpaying. That, in plain English, is where the phrase melt-up comes in.

Revisiting the melt-up scenario matters now because the ingredients look familiar: resilient economic growth, easier financial conditions, massive enthusiasm around artificial intelligence, heavy concentration in a few market leaders, and a public that keeps learning the same annoying lesson: momentum can stay stronger than common sense for longer than expected. The result is a market setup that looks powerful, profitable, and a little too comfortable in its own reflection.

This article takes a fresh look at what a melt-up really is, why investors keep talking about it, what could push it further, and what could bring it to an abrupt end. Spoiler alert: a melt-up is not the same thing as a healthy bull market. It is more like a bull market after three espressos and a standing ovation.

What Is a Melt-Up, Exactly?

A melt-up is a sharp rise in asset prices driven less by calm, methodical fundamentals and more by momentum, fear of missing out, and a rush of buyers who feel they cannot afford to stay on the sidelines. It often shows up late in a cycle, when valuations are already stretched and the story supporting the rally becomes bigger than the spreadsheet.

That does not mean the story is fake. In fact, the most dangerous melt-ups usually start with a perfectly reasonable idea. Maybe earnings are improving. Maybe interest rates are falling. Maybe a new technology really is changing productivity. The trouble starts when a sound idea turns into a universal excuse for paying almost any price. Markets stop asking, “Is this business good?” and start asking, “What if it goes up another 20% without me?” That is not analysis. That is emotional cardio.

In other words, a melt-up is not simply “stocks going up.” Stocks are allowed to do that. A melt-up is when price action becomes self-reinforcing. Rising prices attract more buyers, which causes more rising prices, which makes every cautious person look foolish right up until caution becomes fashionable again.

Why the Melt-Up Thesis Is Back on the Table

The case for revisiting the melt-up scenario starts with the broader macro backdrop. The U.S. economy has stayed more resilient than many expected, even after a long stretch of inflation worries and rate uncertainty. Corporate America has also remained better funded and more adaptable than the doomsayers predicted. Consumers have not vanished. Business investment has not rolled over. And capital spending tied to AI infrastructure has become one of the market’s favorite engines.

That matters because melt-ups are usually fed by a combination of economic durability and narrative excitement. Today, both are available. On one side, you have the argument that the economy can keep expanding. On the other, you have the belief that AI-related spending will improve productivity, lift margins, and justify premium valuations for the companies building the picks, shovels, and digital railroads of the next cycle.

Then there is the mechanical side of the market. Buybacks remain a meaningful support. Passive inflows continue to direct capital into the largest winners. Index concentration means a relatively small cluster of mega-cap names can do an enormous amount of work for the broader averages. If the leaders stay hot, the indexes can look healthier than the average stock feels. That is one reason melt-up conversations keep returning: the market no longer needs every stock to participate equally for the headline numbers to look spectacular.

The Bullish Case: Why a Melt-Up Could Keep Going

Easier Financial Conditions Can Keep Risk Assets Buoyant

One of the clearest supports for a melt-up is easier financial conditions. When markets believe rates are peaking or likely to move lower, risk appetite tends to improve. Lower borrowing costs help valuations, support investment, and make future earnings look more attractive when discounted back to the present. That may sound technical, but the market hears it as, “Your expensive stock just got a little easier to defend.”

Easier conditions also tend to encourage a reach for return. If cash becomes slightly less compelling and bond yields drift lower, investors start leaning back into equities. Not always carefully. Not always gradually. Sometimes with the grace of a shopping-cart sprint on Black Friday.

AI Optimism Has Created a Powerful Narrative Tailwind

Another reason the melt-up scenario keeps resurfacing is the sheer scale of AI enthusiasm. This is not just a social-media theme or a one-quarter fad. Large companies are spending real money on AI infrastructure, semiconductors, cloud capacity, software integration, and related capital projects. The bullish argument is that this spending will not only lift revenue for a handful of tech giants but also improve productivity across industries.

If that thesis keeps holding, markets may continue rewarding the companies viewed as the most important bottlenecks, platforms, and beneficiaries. And when leadership narrows around businesses with huge cash flow, high margins, and strategic importance, investors often tolerate richer valuations for longer than expected. Expensive can get more expensive. Irritatingly so.

Momentum Itself Becomes a Catalyst

This is the part traditional analysts hate, but it matters. Momentum is not just a byproduct in a melt-up. It is fuel. Once price gains become visible enough, they change behavior. Portfolio managers who were underweight leaders feel pressure to catch up. Individual investors who missed the first leg convince themselves there is still time. Companies benefiting from strong share prices can raise capital more easily, recruit talent more effectively, and reinforce the story that they are winning.

That is why melt-ups can look rational and irrational at the same time. They can start with improving fundamentals and then get stretched by performance anxiety. Nobody wants to be the person who sold too early and then had to explain it at a quarterly review.

A Broader Rally Could Add a Second Wind

Ironically, one thing that could extend a melt-up is a broadening of market participation. If gains spread beyond mega-cap tech into industrials, financials, small caps, or international equities, the rally may begin to look healthier. That can reduce immediate fears of a bubble while pulling in fresh capital from investors who had been waiting for a more balanced market. In that scenario, the melt-up becomes more durable because it no longer relies on one glamorous table at the party.

The Bearish Case: Why the Melt-Up Story Can Turn Messy

Valuations Still Matter, Even If the Market Pretends Otherwise

The biggest risk in any melt-up discussion is simple: price can run ahead of reality. Strong businesses deserve premiums, but premiums are not infinite. When investors assume flawless execution, uninterrupted demand, and perfectly timed policy support, they create a setup with very little room for disappointment.

That is especially important in a market where optimism is clustered around a small group of companies. If expectations are sky-high, “good” results may not be good enough. A company can post excellent earnings and still get punished if the market wanted magic, fireworks, and a handwritten note from the future.

Concentration Risk Makes the Index Look Stronger Than It May Be

One of the defining features of the current environment is concentration. When the largest companies become an unusually large share of total market value, the major indexes can rise even if the average stock lags behind. That creates a strange emotional divide. Headlines say the market is roaring. Many investors look at their diversified portfolios and mutter, “Is it, though?”

Concentration does not automatically cause a downturn, but it does raise fragility. If a narrow group of leaders stumbles, the index-level damage can be larger than investors expect. A melt-up built on a thin foundation is still a thin foundation.

Policy, Inflation, and Credit Can Spoil the Party

Melt-ups do not usually end because investors suddenly become disciplined adults. They end because something changes the cost of optimism. Sometimes it is inflation that refuses to cool. Sometimes it is yields moving the wrong way. Sometimes it is credit spreads widening, signaling that financial markets are no longer as relaxed as equity traders would prefer. Sometimes it is a macro shock that reminds everyone risk was not, in fact, abolished.

That is why revisiting the melt-up scenario requires humility. The bullish setup can remain intact for a while, but it depends on a delicate balance. Growth must stay firm enough to support earnings. Inflation must stay tame enough not to frighten policy makers. Financial conditions must stay easy enough to support rich valuations. If one of those pillars weakens, the market can shift from celebration to interrogation very quickly.

Speculation Can Creep In Around the Edges

Another late-cycle warning sign is the quality of risk-taking. In a healthy rally, investors reward improving profits, stronger balance sheets, and better business models. In a melt-up, that discipline can drift. Speculative corners of the market start waking up. Story stocks run on vibes. Margins for error shrink. Every chart begins to look like a motivational poster for overconfidence.

That does not mean the whole market is doomed. It does mean investors should pay attention to how gains are happening, not just that they are happening.

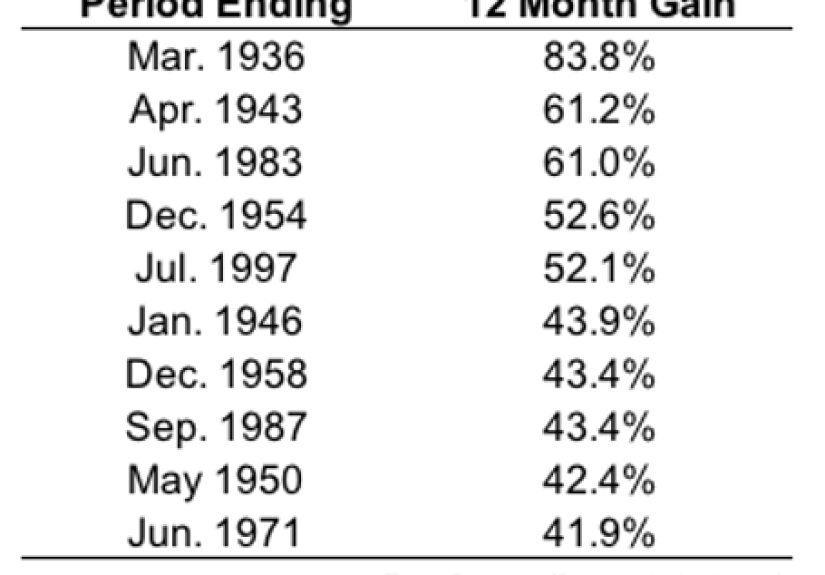

How Melt-Ups Usually End

A melt-up rarely ends with a polite memo. More often, it ends when the market realizes expectations outran evidence. The trigger could be weaker earnings growth, fading AI spending enthusiasm, stickier inflation, higher yields, tighter credit, or a geopolitical shock. Sometimes the spark is tiny. A valuation reset does not need a dramatic recession headline if pricing already assumed near perfection.

It is also common for melt-ups to end in stages. First, leadership narrows. Then volatility rises. Then previously ignored bad news starts mattering again. Finally, investors rediscover words like “discipline,” “diversification,” and “why did I buy that at 38 times sales?”

The lesson is not that investors should run from every strong rally. It is that markets can become vulnerable even while headlines remain cheerful. A market at new highs is not automatically safe just because it looks confident on television.

What to Watch If You Are Revisiting the Melt-Up Scenario

If you want to judge whether the melt-up thesis is gaining strength or losing oxygen, watch a few practical indicators.

- Market breadth: Are more sectors and smaller stocks participating, or are the same few giants doing all the lifting?

- Earnings revisions: Are analysts raising expectations because profits are improving, or are prices rising faster than estimates?

- Valuation spreads: Are leadership groups becoming dramatically more expensive relative to the rest of the market?

- Credit conditions: Are spreads staying tight, or is stress appearing under the surface?

- Rate expectations: Does the market still believe policy will remain supportive?

- Behavior: Are investors chasing quality growth, or chasing whatever moved last Tuesday?

Those signals will not ring a bell at the top. Nothing does. But they help separate a durable advance from a market that is starting to confuse confidence with invincibility.

The Real Takeaway

Revisiting the melt-up scenario is not about predicting a crash with theatrical certainty or declaring that every new high is foolish. It is about recognizing that powerful rallies can be both understandable and unstable. Today’s setup has genuine support: solid corporate balance sheets, continued business investment, easier financial conditions than feared, and a technological story big enough to reshape earnings expectations. That is the rational side.

The unstable side is just as important. Valuations are elevated. Concentration is high. Expectations for AI winners are enormous. Sentiment can change quickly when the market is priced for excellence. That means a melt-up can continue, but it can also become more fragile with every celebratory headline.

The smart response is neither panic nor blind devotion. It is discipline. Respect momentum, but do not worship it. Appreciate innovation, but still ask what is already priced in. Enjoy the rally, but remember that markets are fully capable of turning a beautiful narrative into a very expensive life lesson.

Or, put differently: when the market starts levitating, it is wise to check whether it built wings or just borrowed a trampoline.

Experiences From the Front Row of a Melt-Up

To understand the melt-up scenario, it helps to move beyond charts and into experience. In real life, a melt-up does not feel like a textbook definition. It feels emotional, uneven, and weirdly personal. One portfolio manager may feel pressure because clients keep asking why he owns so much cash. A retirement saver may feel regret every time she sees another headline about record highs. A company executive may feel thrilled that the market loves her sector, while quietly wondering whether expectations have become impossible to satisfy.

Consider the experience of the long-term investor who stayed diversified while a handful of giant stocks ran wild. On paper, that investor did nothing wrong. The portfolio was balanced, sensible, and built for decades rather than months. But during a melt-up, sensible can feel unbearably slow. Every dinner conversation includes someone who bought the hottest names and suddenly sounds like a market prophet. The disciplined investor starts asking dangerous questions, not because the plan failed, but because someone else got rich faster. That is one of the most underestimated pressures in a melt-up: envy dressed up as strategy.

Then there is the adviser trying to talk clients off the emotional ledge. In one week, the adviser hears two opposite demands. One client wants to sell everything because valuations look absurd. Another wants to pile into the winners because “this time the technology is real.” Both clients may be partly right and partly reckless. The adviser’s real job becomes emotional translation. He has to explain that expensive markets can keep rising, but that chasing them without risk controls is not a plan. During a melt-up, good advice often feels unsatisfying precisely because it refuses to tell a dramatic story.

Executives live through their own version of this. When your company operates near a hot theme, a rising stock price can be wonderful and dangerous at the same time. Employees feel wealthier. Recruiting gets easier. Investors become friendlier. But the bar moves higher every quarter. A merely strong result can disappoint if the market expects perfection. In that environment, management teams can feel as though they are running on a treadmill that speeds up every time they hit their numbers.

Retail investors often describe a melt-up with one phrase: “I felt late.” That feeling matters because it changes behavior. People stop asking whether an asset is attractive and start asking whether there is still time. They buy on headlines. They average up without a framework. They convince themselves that missing out is the only real risk. Later, if the market snaps back, they discover there was another risk after all. It had their name on it.

The most grounded experience, oddly enough, often belongs to the investor who has lived through a few cycles already. That person may still participate in the rally, but with less drama. They know strong markets can continue longer than expected. They also know excitement is not a valuation metric. Their advantage is not genius. It is memory. They remember that melt-ups can feel exhilarating right before they become educational.