Table of Contents >> Show >> Hide

- What Do We Even Mean by a “Normal” Market?

- Interest Rates: Rarely Hanging Out in the Middle

- Valuations: Average Is More of a Myth

- Returns: The 10% Average You Rarely Actually See

- Why We Crave “Normal” Even When It Almost Never Happens

- Markets Aren’t NormalBut They’re Not Random Chaos Either

- What “Abnormal” Markets Mean for Real Investors

- How Often Are Markets “Normal”? Almost Neverand That’s Okay

- Real-World Experiences: Living Through “Abnormal” Markets

If you’ve ever said, “I’ll invest when the market goes back to normal,” I have bad news:

you might be waiting longer than it takes for the DMV to call your number. In finance,

“normal” is one of those comforting words we use to describe a world that almost never exists.

The idea behind “normal markets” sounds simple enough: interest rates in a reasonable range,

stock valuations near long-term averages, and annual returns that quietly land around 10%,

like a well-behaved golden retriever. But when you look at the data, the market behaves

more like a hyperactive border collie who just found an espresso machine.

Inspired by Ben Carlson’s piece on A Wealth of Common Sense, this article digs into

how often markets are actually “normal,” why averages are so misleading, and what investors

can learn from the fact that financial markets spend most of their time being anything but

average.

What Do We Even Mean by a “Normal” Market?

Before we can ask how often markets are normal, we need a working definition. Typically,

investors think of “normal” in three ways:

- Interest rates sitting in a familiar historical range.

- Valuations (like the CAPE ratio or P/E ratio) hovering around long-term averages.

- Annual returns landing somewhere near the long-term stock market average of about 10%.

In textbook statistics, a “normal distribution” (that smooth bell curve you met in high school)

says that about 68% of outcomes should fall within one standard deviation of the mean and 95%

within two standard deviations. In other words, most results cluster reasonably close to the

average.

That’s great in theory. In practice, financial markets didn’t read the textbook.

Stock returns show fat tails, frequent outliers, and extreme years that happen far more often

than a simple bell curve would predict. So even if we try to define “normal” using averages and

standard deviations, markets politely smile and do something completely different.

Interest Rates: Rarely Hanging Out in the Middle

Let’s start with bond yields, a favorite yardstick for “normalcy.” Looking back to the late 19th

century, the average yield on the 10-year U.S. Treasury has been around 4.6%. If you call

“normal” a range of 4–6%, that sounds reasonable. Mid-single-digit yields, not too hot,

not too cold.

The historical data, however, show that 10-year Treasuries have only lived in that 4–6% band

roughly a quarter of the time over more than 140 years. Most of the time, rates are either:

- Much lower – Think post–Global Financial Crisis and the 2020 pandemic era, when yields hovered near zero.

- Much higher – Think 1970s and early 1980s, when double-digit yields were a thing and mortgage rates could make grown adults cry.

So even if 4–6% feels like the “normal” bond world we were promised in textbooks and retirement

calculators, historically it’s been more of a vacation home than a permanent address. Interest

rates spend most of their time either well below or well above that cozy middle.

Valuations: Average Is More of a Myth

Stock valuations are another place where people love to talk about “normal.” One of the most

common valuation measures is the cyclically adjusted price-to-earnings ratio (CAPE), which looks

at price relative to the average of 10 years of inflation-adjusted earnings.

Since the late 1800s, the average CAPE ratio for U.S. stocks has been around 16. If you call

“normal” anything between 15 and 17, you might expect the market to live in that neighborhood

quite a bit. After all, that’s the long-term average, right?

In reality, the CAPE ratio has only been in that 15–17 band roughly 14% of the time over

more than a century of market history. The rest of the time, valuations have been:

- Below average during crises, panics, and periods of pessimism.

- Above average during booms, bubbles, and everything that came with low interest rates and high optimism.

Investors often say, “I’ll buy when valuations go back to normal.” The historical record suggests

that “normal” is more of a narrow hallway the market sprints through on its way from “cheap”

to “expensive” and back again.

Returns: The 10% Average You Rarely Actually See

The long-term average annual return for U.S. stocks (using the S&P 500 as a proxy) is close

to 10% per year. This number is famous. It shows up in retirement calculators, marketing

brochures, and suspiciously optimistic Twitter threads.

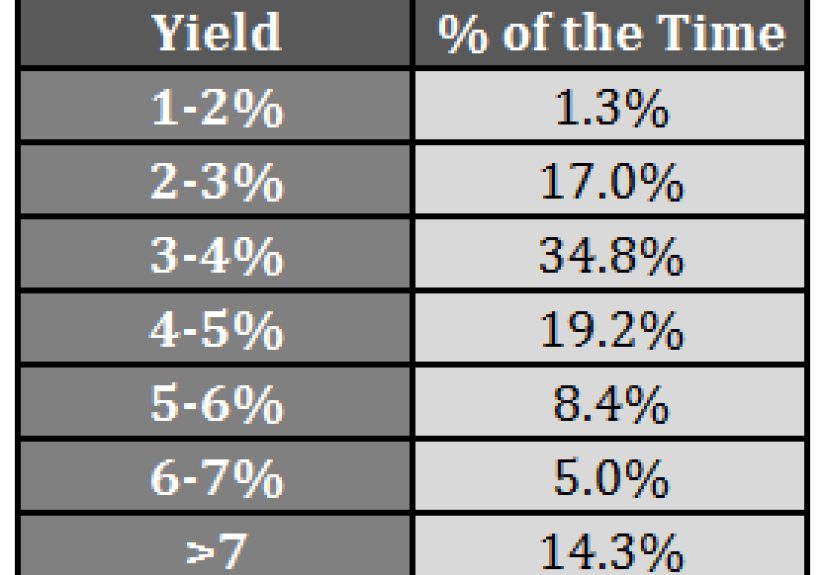

Here’s the twist: if you define “normal” as a year when the S&P 500 returns somewhere

between 8% and 12%in other words, roughly around that 10% averagethe market has only

landed in that range a tiny fraction of the time. Since the late 1920s, the S&P 500 has

finished a year in the 8–12% band only about three times. That’s roughly 3–4% of all years.

Most of the time, returns are nowhere near average. Instead, they look like:

- Big up years – +20%, +30% or even more in strong bull markets.

- Ugly down years – -20% or worse when recessions and crises hit.

- Sideways chop – years where the index goes nowhere, but your emotions get a full workout.

If you plot annual returns, you don’t get a neat bell curve centered calmly around 10%.

You get a lumpy, uneven distribution with lots of extreme outcomes. Technically, the average

is still about 10%, but you almost never get anything actually close to it in any single year.

Why We Crave “Normal” Even When It Almost Never Happens

If markets so rarely behave normally, why is everyone obsessed with getting back to

“normal conditions”?

A big reason is psychological comfort. Humans like stability, predictability, and patterns.

A world where interest rates, valuations, and returns line up neatly with long-term averages

feels safe. We picture a scenario where:

- Bonds yield “something fair,”

- Stocks are “reasonably priced,” and

- Our portfolios quietly grow at 8–10% per year without drama.

The problem is that this picture is more fantasy than reality. Economic regimes change.

Inflation cycles come and go. Technology shifts the earnings power of companies. Central

banks experiment with interest rate policies. Global crises show up uninvited. Markets are

constantly reacting to new information.

In that kind of world, “normal” is less of a destination and more of a fleeting moment that

passes by while everyone is arguing on financial TV.

Markets Aren’t NormalBut They’re Not Random Chaos Either

If markets don’t behave like a neat normal distribution, does that mean they’re totally

unpredictable chaos? Not exactly.

Over longer time horizons, certain patterns do emerge:

-

Stocks tend to reward long-term investors.

Decades of data show that diversified equity investors have usually been rewarded

for staying invested, even if the path was bumpy. -

Volatility clusters.

Big up and down days tend to show up in bunchesespecially during crisesrather than

being evenly sprinkled through time. -

Bad years are the cost of good long-term returns.

Those scary drawdowns are often the “fee” you pay to access equity-like returns over time.

So while returns don’t line up with a classic bell curve, they also aren’t static noise.

Markets have a logicjust not a tidy, classroom-friendly one.

What “Abnormal” Markets Mean for Real Investors

If normal market conditions are so rare, the practical question is: what should investors

actually do with this information?

1. Stop Waiting for the Perfect Entry Point

Many people sit on the sidelines waiting for markets to “settle down,” interest rates to

“normalize,” or valuations to return to some perceived fair value. The problem is that by

the time things feel comfortable again, prices often already reflect that comfort.

Instead of hunting for a perfect, normal moment, strategies like dollar-cost averaging

can help you invest through different environments without trying to outsmart the cycle.

You accept that sometimes you’ll buy when the market looks expensive, sometimes when it

looks cheapand over time, you capture the journey instead of trying to time the snapshot.

2. Build Plans That Assume Volatility, Not Normalcy

Retirement plans and investment goals shouldn’t assume smooth, normal returns every year.

They should be built around ranges and probabilities:

- What happens if returns are below average for a decade?

- How does your plan handle multiple negative years in a row?

- Are you over-relying on a single asset class behaving “normally”?

Using conservative assumptions and stress-testing your plan helps make sure your strategy

can survive reality, not just the textbook version of reality.

3. Respect Risk Instead of Assuming the Bell Curve Has Your Back

A lot of risk models assume some flavor of normal distribution, even if everyone knows

markets aren’t perfectly normal. That’s not uselessbut it can be dangerous if you treat

those models as guarantees.

Extreme events happen more often than a simple bell curve would suggest. That’s why it’s

crucial to:

- Diversify across asset classes and regions.

- Avoid excessive leverage.

- Maintain a reasonable cushion in safer assets for short-term needs.

Planning for non-normal markets means accepting that “tail events” aren’t rare once-in-a-lifetime

freak accidentsthey’re part of the long-term landscape.

4. Embrace the Idea That “Abnormal” Is Actually Normal

One of the most helpful mindset shifts is this: it’s more normal for markets to be

not normal.

When you accept that:

- Valuations will swing from cheap to expensive.

- Returns will leap from great to terrible and back again.

- Volatility will arrive suddenly and leave slowly.

…you’re less likely to panic when the inevitable happens. Instead of thinking, “Something is

broken,” you can think, “This is uncomfortable, but it’s part of how markets work.”

How Often Are Markets “Normal”? Almost Neverand That’s Okay

When you zoom out, a clear pattern emerges:

- Interest rates have spent relatively little time in “normal” mid-range zones.

- Stock valuations almost never sit neatly at long-term averages.

- Annual returns rarely land close to the famous 10% number.

The averages we quote so often10% stock returns, mid-single-digit bond yields, fair

valuationsare useful for long-term planning. But they’re not a description of what you’ll

see in any given year. They’re the result of a long, messy history of markets overshooting

and undershooting those averages over and over again.

The takeaway for investors is simple but not always easy:

stop waiting for “normal” and start building strategies that can handle the abnormal.

Because in real-world markets, “abnormal” is the baseline.

Real-World Experiences: Living Through “Abnormal” Markets

It’s one thing to talk about abnormal markets in terms of charts and statistics. It’s another

to live through them with your money on the line. Let’s walk through what “normal” almost

never looks likeand what real investors have actually experienced over the last few decades.

The Tech Bubble: When “Normal” Was Overheated

In the late 1990s, the stock market looked anything but normal. Valuations soared, especially

for tech companies with little or no profits. Expectations were sky-high. Many investors

convinced themselves that this was the new normal: double-digit annual gains, innovation

everywhere, and a world where you could slap “.com” on a company name and watch its stock

price rocket.

When the bubble finally burst in 2000, the following years delivered a harsh reminder that

mean reversion is very real. The market went from euphoric to bruised. Investors who had

assumed that the late 1990s returns were the baseline for the future discovered that a few

very “abnormal” years had just inflated long-term averages.

The Global Financial Crisis: “Normal” Goes Out the Window

Fast forward to 2008–2009. Housing markets collapsed, major financial institutions wobbled,

and global markets took a nosedive. This period didn’t just feel abnormalit felt surreal.

Huge daily moves in stock prices, credit markets freezing, and headlines that sounded like

they had been pulled from a disaster movie.

Investors who had built their expectations around smooth 8–10% annual returns suddenly faced

drawdowns that challenged their time horizons and their nerves. Those who sold out during the

panic often locked in losses. Those who stayed invested (or even rebalanced into risk assets)

eventually benefited from the recovery that followedbut there was nothing “normal” about

the journey.

The Post-Crisis Era: Low Rates, High Valuations, and New “Normals”

After the crisis, central banks kept interest rates unusually low for an extended period.

Bond yields sat at levels that would have seemed impossible a few decades earlier. At the

same time, equity valuations rose as investors were pushed into risk assets in search of

return.

For younger investors, this environmentlow rates, rising stock markets, and frequent

headlines about “all-time highs”started to feel normal. But historically, it was another

unusual regime: a long stretch where policy interventions, low inflation, and abundant

liquidity shaped outcomes in a way that was very different from many earlier episodes.

The 2020 Pandemic Shock: A Crash and Rally Rolled Into One

When the COVID-19 pandemic hit in early 2020, global markets reacted violently. Stocks fell

at historic speed, volatility spiked, and the sense of uncertainty was enormous. For a brief

period, it felt like the financial world was reliving 2008 in fast-forward.

Then, almost as quickly, markets rebounded. Massive fiscal and monetary support, rapid

changes in behavior, and optimism about recovery fueled a sharp V-shaped bounce. The year

ended with markets posting surprisingly strong returns, which would have looked completely

out of place if you had only watched the news during the March panic.

If you tried to map 2020 onto a “normal” template for market behavior, good luck. It was a

year that reminded investors that markets can be both terrifying and rewarding in a very

short span of time.

Lessons from Abnormal Decades

Looking at these episodes together, a pattern emerges:

- Some decades (like the 1980s and 1990s) deliver spectacular returns.

- Others (like the 2000s) are flat or disappointing overall.

- Individual years can be wildly positive or deeply negative, often clustered around periods of economic change.

Yet when you string all those wild, uneven years together, you still end up with long-term

averages that look surprisingly tidy on paper. That’s the strange irony of market history:

the path is chaotic, but the destination often looks smooth.

For real investors, the challenge is learning to live with that chaos without letting it

derail your plan. That means:

- Accepting that abnormal events are part of normal market life.

- Sticking with diversified portfolios through uncomfortable periods.

- Focusing more on time in the market than on perfectly timing the market.

In the end, “How often are markets normal?” is almost the wrong question. A better one

might be: “How can I build an investment strategy that still works when markets are

not normal?” Because if history is any guide, that’s the world you’re actually

investing in.