Table of Contents >> Show >> Hide

- What Is a Bond Market Correction, Exactly?

- Why Bond Market Corrections Happen

- A Brief History of Bond Market Corrections

- What Bond History Really Tells Investors

- Practical Lessons for Today’s Bond Investors

- Experiences and Real-World Takeaways from Bond Corrections

- Conclusion: Using History to Stay Sane About Bonds

If you’ve ever been told that bonds are “the boring, safe part” of your portfolio, the last few decades have probably felt like a prank.

From surprise rate hikes in the 1990s to the historic bond sell-off of 2021–2022, the bond market has had more plot twists than a prestige TV show.

Yet, as messy as bond market corrections can be, they also come with patterns, probabilities, and plenty of lessons for long-term investors.

Inspired by the kind of clear, no-nonsense perspective you’ll find on the

personal finance blog A Wealth of Common Sense, this article walks through a history of bond market corrections,

why they happen, how bad they’ve really been, and what investors can reasonably expect going forward.

We’ll also finish with some real-world experiences and practical takeaways so you can look at your bond allocation with a little more calm

(and maybe even a little more optimism).

What Is a Bond Market Correction, Exactly?

With stocks, a “correction” usually means a drop of 10–20% from a recent high. Bonds are different:

they’re typically less volatile, so a “correction” in the bond market often refers to a meaningful drawdown in prices,

especially in longer-term bonds, over a relatively short period.

Think of it this way:

- Bond prices fall when interest rates rise.

- The longer the bond’s maturity (and the higher its duration), the more sensitive it is to rate moves.

- Corrections show up as negative total returns (price drops that temporarily overwhelm interest income).

A bond correction might be:

- A sharp, single-year loss in long-term Treasuries or corporates.

- A multi-year period where bond total returns are negative or barely positive after inflation.

- A broad, global bond sell-off driven by rising yields and inflation fears.

The key is that these aren’t just tiny blips. They’re periods when supposedly “safe” bonds suddenly feel risky,

investors question their assumptions, and financial headlines light up with phrases like “bond rout,” “massacre,” or “bear market.”

Why Bond Market Corrections Happen

Bond corrections usually trace back to a few familiar culprits:

1. Interest Rate Shocks

Central banks, especially the Federal Reserve, are the main characters in most bond dramas.

When they raise short-term rates faster or higher than markets expect, long-term yields can jump,

and bond prices fall in a hurry. This is what happened in 1994 and again in 2022,

when aggressive rate hikes shocked markets after a long period of low yields.

2. Inflation Surprises

Bonds are promises to pay fixed cash flows in the future. When inflation comes in hotter than expected,

those future dollars are suddenly worth less. Investors demand higher yields to compensate,

which means lower bond prices today. The inflation surge after the pandemic is a textbook example.

3. Changes in Risk Perception

In credit markets (corporate bonds, high-yield, emerging markets), corrections can stem from fears about defaults,

recessions, or balance sheet weakness. Spreads widen, prices fall, and total returns can take a hit even if Treasury yields are stable.

4. Positioning and Leverage

When investors have loaded up on long-duration bonds or leveraged strategies that depend on stable or falling yields,

a sudden rate spike can trigger forced selling. That selling, in turn, can deepen the correction,

even if the underlying economic story doesn’t look apocalyptic.

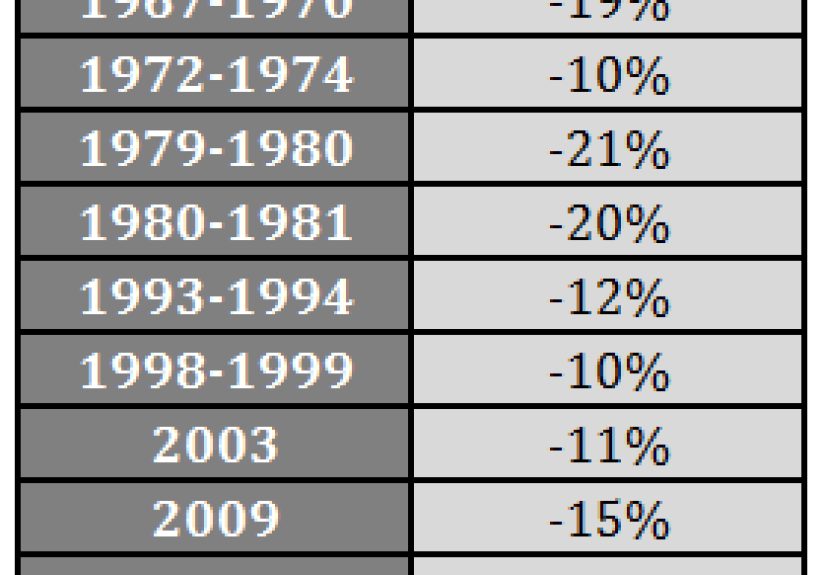

A Brief History of Bond Market Corrections

While most investors focus on stock crashes, the bond market has its own set of war stories.

Let’s walk through a few of the big episodes that still influence how professionals think about bond risk today.

The Great Inflation and the Volcker Era (1970s–early 1980s)

In the 1970s, inflation steadily eroded the purchasing power of bond coupons.

Yields soared into double digits, and existing bond prices were crushed.

The early 1980s, under Fed Chair Paul Volcker, brought extremely high short-term rates in an effort to break inflation.

For existing bondholders, it was painful. For long-term investors willing to buy at those yields,

it was a once-in-a-generation opportunity.

Lesson: high inflation plus rising rates is the worst combination for bonds in the short term,

but the resulting high yields can set up excellent long-term returns.

1994: The Original “Bond Massacre”

The 1994 bond correction is often cited as the modern benchmark for bond pain before the 2020s.

The Fed surprised markets with a rapid series of rate hikes after a long period of relative calm.

Long-term Treasury and municipal bonds posted sizable negative returns, and leveraged bond strategies

especially those using derivatives and structured productstook heavy losses.

The big takeaway from 1994 was not that bonds are “dangerous,” but that term risk and leverage can bite hard

when the interest-rate regime changes unexpectedly.

2008–2009: Bonds in the Global Financial Crisis

The 2008 financial crisis was primarily a credit and equity meltdown, but the bond market story was more nuanced:

- High-quality U.S. Treasuries rallied as investors fled to safety.

- Corporate bonds and asset-backed securities, especially those linked to mortgages, were hammered.

- Liquidity evaporated in some niches, pushing prices down far more than default risks alone would suggest.

Here, the “correction” wasn’t about rising yields across the board; it was about credit risk and liquidity risk,

and it reminded investors that “bond” is not synonymous with “risk-free.”

2013: The “Taper Tantrum”

In 2013, the Fed hinted it would start tapering its quantitative easing (QE) bond purchases.

That was enough to spook markets. Long-term Treasury yields jumped quickly, and the prices of

long-duration bonds fell. While the drawdown was modest compared with later events,

it was a loud reminder that the bond market is forward-lookingand allergic to surprises.

Investors learned (again) that when your strategy depends on central banks continuing to buy bonds indefinitely,

your risk is not just “interest rate risk”it’s “policy disappointment risk.”

2020–2023: The Worst Bond Bear Market in Modern History

The pandemic era delivered a unique sequence:

- In early 2020, Treasury yields plunged as the world rushed into safe assets.

- Massive fiscal stimulus, supply-chain disruptions, and reopening effects drove inflation higher than expected.

- Starting in 2022, the Fed and other central banks launched one of the fastest rate-hike cycles in decades.

The result was brutal for bondholders. Yields surged from near-zero to levels not seen in many years.

Global bond indexes fell more than 20% from their peaks, marking the first true global bond bear market in a generation.

Many core bond funds posted back-to-back negative years, something that had been vanishingly rare historically.

For investors who had piled into bonds during the zero-rate era, it felt like the asset class

that was supposed to stabilize portfolios had suddenly turned against them.

For long-term investors willing to look forward, the silver lining was clear: starting yields finally became attractive again.

What Bond History Really Tells Investors

When you zoom out, a few key themes emerge from decades of bond market corrections and recoveries.

1. Income Is the Real Engine of Long-Term Returns

Over long periods, most of a bond portfolio’s total return comes from the interest income,

not from price changes. When yields rise during a correction, that hurts in the short termbut it improves

the outlook for future returns. If you reinvest your coupons and stay invested, higher yields eventually work in your favor.

2. Duration Cuts Both Ways

Longer-duration bonds:

- Benefit more when yields fall (bigger price gains).

- Get hit harder when yields rise (bigger price losses).

Shorter-duration bonds are less exciting but far less sensitive to rate shocks.

Many investors have learnedsometimes the hard waythat reaching for yield via long-duration bonds

can be painful when the interest-rate cycle turns.

3. Diversification Still Matters

In most historical crises, high-quality bonds have held up better than stocks,

even when they experienced their own corrections. The 2021–2022 period was a rare case when both stocks and bonds struggled at the same time,

but that doesn’t erase the long-term evidence that diversified stock–bond portfolios have historically smoothed the ride compared with stocks alone.

4. Regimes Change, but Risk Never Disappears

The story of bond market corrections is really a story about changing regimes:

- The high-inflation, high-yield era of the 1970s and early 1980s.

- The multi-decade bond bull market from the mid-1980s to around 2020.

- The sharp reset higher in yields starting in 2021–2022.

In each regime, investors were tempted to extrapolate the present into the future.

In practice, the future kept surprising them. The only constant has been that bonds involve trade-offs:

less long-term volatility than stocks, but still very real short- and medium-term risks.

Practical Lessons for Today’s Bond Investors

So what can we learn from this history if we’re trying to manage bond risk with a little “common sense” today?

Match Your Bonds to Your Time Horizon

If you need money in a few yearsfor a down payment, tuition, or early retirement expenses

parking that cash in very long-duration bonds can be risky. Shorter-duration government or high-quality investment-grade bonds

may offer less yield, but their price swings are more manageable, especially during rapid rate moves.

Think in Terms of Real, Not Just Nominal, Returns

A 6% yield sounds great until inflation is running at 7%. A 3% yield can be perfectly fine if inflation sits at 2%.

Historically, many painful bond corrections have been linked to inflation surprises,

so paying attention to inflation trendsand not just nominal yieldsis essential.

Accept That Corrections Are Features, Not Bugs

Just as stock investors have to live with bear markets, bond investors have to live with corrections.

You can’t earn a yield premium without occasionally enduring volatility.

What matters is whether your allocation matches your goals and risk tolerance,

not whether you picked the perfect moment to buy.

Avoid Overconfidence in “Safe” Assets

The 1994 bond sell-off, the 2013 taper tantrum, and the 2021–2022 bond bear market all punished investors

who assumed that bonds “can’t lose much.” They canespecially when they’re long term,

concentrated in one sector, or financed with leverage.

A truly conservative strategy uses bonds thoughtfully, not blindly.

Experiences and Real-World Takeaways from Bond Corrections

Beyond charts and return series, the most valuable lessons from bond market corrections often come from lived experience

how real investors and advisors felt, reacted, and adjusted when their “safe” assets suddenly stopped behaving.

Investors who lived through the 1994 correction often describe it as a turning point in how institutions manage interest-rate risk.

Back then, many portfolios were built on the assumption that bonds wouldn’t move all that much.

When long-term yields jumped and prices fell sharply, it exposed how fragile leveraged bond strategies and

complex derivatives could be when the rate environment changed quickly.

Some pension funds and insurers walked away from that period with a new respect for duration risk and stress testing.

Fast forward to the global financial crisis of 2008, and many individual investors made a different discovery:

not all bonds are created equal. High-yield and structured credit products that had been marketed as “safe income solutions”

behaved more like stocksplunging in price as credit fears exploded.

By contrast, plain-vanilla Treasuries often rose, cushioning the blow for diversified portfolios.

Advisors who had stuck to a core of high-quality bonds found it easier to keep clients invested through the turmoil.

The most emotionally challenging bond experience for many investors, however, came after the pandemic,

when inflation spiked and central banks raised rates aggressively.

Investors who had piled into long-term bonds or broad bond funds while yields were near zero

suddenly watched “safe” holdings post losses that looked more like equity drawdowns.

For retirees or near-retirees, this was especially uncomfortable:

they weren’t just reading about volatility in a textbook; they were living through sequence-of-return risk in real time.

Yet those same years also provided some crucial perspective.

Investors who had the flexibilityand disciplineto stay invested,

reinvest coupons, or rebalance into bonds at higher yields suddenly found themselves in a very different environment.

Instead of wondering how to squeeze income out of a 1% bond market,

they were able to lock in much more attractive yields with the same or less risk.

In conversations with advisors and planners, this shift often shows up as a quiet realization:

the pain of a bond correction is front-loaded, while the benefits of higher yields are back-loaded.

Another recurring theme from practitioner experience is the value of clear expectations.

Investors who were told, “Bonds never lose money,” were understandably shaken by double-digit drawdowns.

Investors who were told, “Bonds are generally less volatile than stocks, but they can and will go through corrections,”

tended to handle the same environment with more composure.

In practice, the difference comes down to framing: treating bonds as tools with specific trade-offs,

rather than as magical shock absorbers.

Finally, many advisors now use the history of bond corrections as a teaching tool.

They show clients that the worst bond drawdowns, while painful, have been finite;

that rising yields eventually improve prospective returns;

and that diversified portfoliosincluding a mix of stocks, bonds, and possibly other assetsstill provide

more resilience than making all-or-nothing bets on any single asset class.

That perspective doesn’t make a correction feel good in the moment,

but it can keep investors from turning a temporary setback into a permanent loss by abandoning a sound plan.

Conclusion: Using History to Stay Sane About Bonds

Bond market corrections are not glitches in the systemthey’re the price investors pay for the stability and income

that bonds offer over the long run. From the Volcker era to the bond “massacres” of 1994 and 2022,

each episode has reinforced a few core truths: interest rates are unpredictable, inflation matters,

and even “safe” assets come with trade-offs.

The good news is that history also shows bonds recovering,

income eventually overpowering price declines, and diversified investors coming out the other side with their long-term goals intact.

If you handle your bond allocation with a bit of common sensematching duration to your horizon,

respecting inflation risk, and avoiding overconfidenceyou don’t have to fear bond market corrections.

You can study them, plan around them, and, when yields finally move higher, even use them to your advantage.