Table of Contents >> Show >> Hide

- Median Net Worth: The Number That Doesn’t Care About Billionaires

- Why “Alarmingly Low” Can Be True Even If the Median Isn’t Tiny

- The Wealth Distribution Problem: A Steep Cliff, Not a Gentle Hill

- Debt: The Quiet Net-Worth Eater With a Megaphone

- The “Emergency Test” Shows Why Net Worth Can Feel Low

- What’s Driving the Median Down (or Keeping It From Rising Faster)

- How Households Build Net Worth When the Median Feels Depressing

- So… Is the Median Net Worth “Alarmingly Low”?

- Experiences That Make the Median Net Worth Feel Low (Real-Life Snapshots)

- 1) The renter who’s doing everything rightand still can’t get traction

- 2) The new homeowner who’s “wealthy” on paper but feels broke in practice

- 3) The debt juggling act that quietly reshapes the future

- 4) The caregiver household where time is the scarce resource

- 5) The “middle” household that looks stable until one shock hits

If you’ve ever looked at a headline about “record household wealth” and thought, “Cool… so why does my bank account still feel like it’s doing hot yoga in a sauna?”

you’re not imagining things. America can be rich and feel broke at the exact same time. The trick is that the country’s wealth is not evenly spread out

it’s more like a pizza where one table ordered extra cheese, the other table got one lonely olive, and someone is arguing over who “technically” tipped.

That’s where median net worth comes in. It’s the financial “middle seat” of America: half of households have more net worth than the median,

and half have less. And when you look at that middle number, it’s hard not to gulp a little. Not because the median is “zero,” but because the median

often doesn’t translate into everyday stabilitythe kind where a surprise car repair doesn’t turn into a three-month soap opera of credit card interest.

Let’s unpack what the median net worth really is, why it can be surprisingly low compared to the cost of modern life, and what this tells us about

the real financial health of American householdsbeyond the glossy “the stock market is up” vibe.

Median Net Worth: The Number That Doesn’t Care About Billionaires

What net worth actually means

Net worth is your assets minus your debts. Assets can include cash, a home, retirement accounts, vehicles, and investments.

Debts include mortgages, credit cards, student loans, auto loans, and that “zero interest” furniture purchase that mysteriously became not zero interest.

The result can be positive, negative, or “please don’t make me log in to check.”

Why the median matters more than the average

The average (mean) gets yanked upward by the ultra-wealthy. If one household has $50 and another has $50 million, the average says,

“Congrats, you’re both basically millionaires.” The median is harder to bully. It tells you what the typical household looks like,

not what happens when a hedge fund manager walks into the room and everyone suddenly “averages” into prosperity.

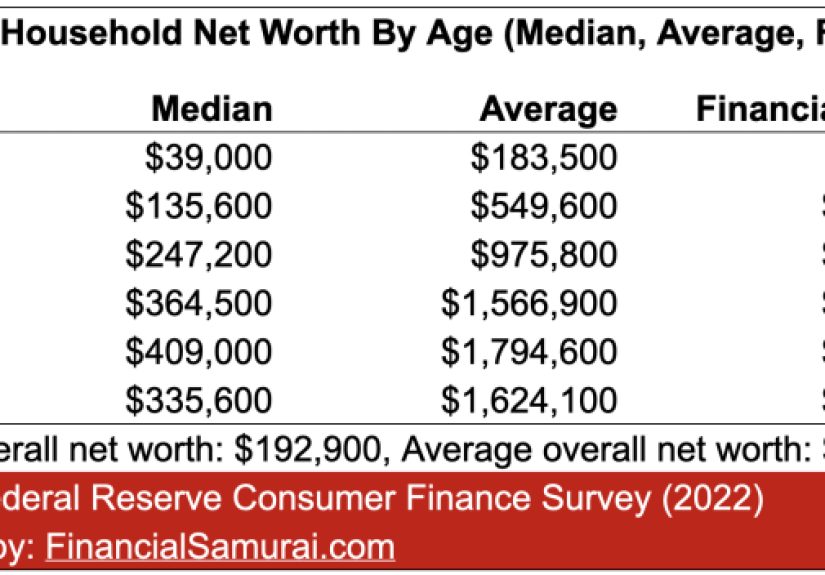

So what is the median net worth?

Depending on the dataset, the median household wealth/net worth in the early 2020s is roughly in the neighborhood of $190,000.

That sounds like a lot until you remember two crucial details:

- Net worth is not the same as cash. A big chunk may be trapped in home equity or retirement accounts.

- The distribution is steep. “Middle” does not mean “comfortable,” especially with modern costs and debt loads.

In other words, the median can look decent on paper while still representing a household that’s one medical bill, layoff, or rent hike away from

performing interpretive dance titled “I Shouldn’t Have Bought That Air Fryer.”

Why “Alarmingly Low” Can Be True Even If the Median Isn’t Tiny

Because the median includes home equity (and many people don’t own homes)

Homeownership has historically been the main wealth engine for middle-class families. When home values rise, homeowners’ net worth can riseoften

without them doing anything except paying a mortgage and trying not to think about property taxes.

But plenty of households rent. And renters typically have far less net worth than homeowners. If your biggest asset is “the security deposit you hope

to see again,” your net worth story will look very different from someone building equity.

Because net worth can be “illiquid wealth”

A household can have a respectable net worth and still feel financially fragile. Imagine:

- $140,000 in home equity

- $70,000 in retirement accounts

- $5,000 in checking/savings

- $18,000 in high-interest debt

On paper, net worth looks fine. In real life, you can’t pay the electric bill with “retirement vibes,” and tapping home equity isn’t always quick,

cheap, or even possible.

Because the cost of “normal life” has gotten expensive

One reason median net worth feels low is that major life milestones cost a lot more now. Housing is the loudest example. When the median existing-home

price is over $400,000, a median net worth around $190,000 doesn’t scream “easy down payment” once you factor in moving costs, closing costs,

interest rates, and the reality that you still need food and health insurance after you buy the house.

And it’s not just housing. A household can have a positive net worth while still struggling with day-to-day cash flow because monthly obligations

don’t politely wait for your “wealth” to become liquid.

The Wealth Distribution Problem: A Steep Cliff, Not a Gentle Hill

The bottom half holds a tiny slice of the pie

One of the most sobering realities is how concentrated wealth is. When the bottom half of households collectively hold only a small share of total

wealth, the median can’t rise dramatically unless that bottom half is truly building assetsnot just treading water.

This is why national “record wealth” headlines can coexist with very real financial strain. A strong stock market mainly boosts households that own

substantial financial assets. If you don’t have much invested, you don’t get much lift.

The median hides giant differences by age, education, and race

Median net worth is one number, but America is a collection of different financial realities:

- Age: Younger households often have lower net worth because they’re early in the asset-building journey (and frequently carrying debt).

- Education: Higher education is associated with higher wealth, but student debt can delay the climb.

- Race and ethnicity: Persistent wealth gaps reflect long-term differences in homeownership, income, intergenerational transfers, and access to opportunity.

The takeaway isn’t that any one group is “doing it wrong.” It’s that wealth is built over time through assets that appreciate (homes, investments),

and access to those assets has not been equal.

Debt: The Quiet Net-Worth Eater With a Megaphone

Household debt has been rising

Debt isn’t automatically bad. Mortgages can build equity. Student loans can increase earnings. Even auto loans can be a practical tool when the

alternative is walking 12 miles to work while carrying a printer.

The problem is costly debt (especially revolving credit) and debt taken on to cover basics. High interest rates can turn

“I’ll pay it off soon” into “I now have a long-term relationship with my credit card company.”

Debt payments squeeze the ability to save

When a larger share of income goes to required paymentsmortgages, rent, car payments, minimum credit card paymentsless is left over to build

emergency savings or invest. That slows net worth growth for the households that most need it.

This is the wealth-building treadmill: you’re moving, you’re working hard, you’re sweating… and somehow the scenery isn’t changing.

The “Emergency Test” Shows Why Net Worth Can Feel Low

A $400 surprise is still a big deal for many households

A classic way to measure real-world financial resilience is the “unexpected expense” question. If a household can’t handle a relatively modest

surprise cost without borrowing, it signals that their financial cushion is thinregardless of what their net worth looks like on paper.

And because modern life is basically a subscription service for surprise expenses (car repair, dental bill, broken phone, flight change fee),

thin cushions create chronic stress.

Rainy-day savings are not universal

Another resilience marker is whether people have enough set aside to cover a few months of expenses if income drops. If you don’t, a job disruption

can quickly turn into debt, missed payments, or draining retirement accountsmoves that can shrink net worth fast.

What’s Driving the Median Down (or Keeping It From Rising Faster)

1) Late starts on asset ownership

If you’re buying a home later, investing later, or delaying retirement contributions because you’re paying for rent, childcare, or debt,

your wealth-building timeline compresses. Meanwhile, the households already holding appreciating assets keep compounding.

2) High-cost credit used for essentials

When credit cards become a bridge for groceries, utilities, or medical costs, interest can grow faster than savings. That doesn’t just slow wealth

growthit can reverse it.

3) Income that rises slower than key expenses

Even moderate inflation can matter when the biggest categorieshousing, insurance, healthcare, food away from homedon’t politely stay in their lane.

Households can feel “behind” even if their wages increased, because the price of being a functional adult increased too.

4) Unequal access to “wealth accelerators”

Wealth accelerators are things like employer retirement matches, stable benefits, homeownership in a rising market, or the ability to invest regularly.

If you don’t have access to these, you can do everything “responsibly” and still build wealth much more slowly.

How Households Build Net Worth When the Median Feels Depressing

This isn’t a “skip lattes and you’ll own a yacht” lecture. Building net worth is often about consistent, unglamorous actionsplus a little luck and

a lot of time. But there are patterns that tend to matter:

Focus on the big levers

- Emergency buffer: Even a small cushion can prevent expensive debt spirals.

- High-interest debt: Reducing costly interest is like giving yourself a raise.

- Retirement match: If available, it’s one of the few “free money” deals left in polite society.

- Automated saving/investing: Consistency beats perfection.

- Skills and earnings growth: Higher income can make saving possible, but only if lifestyle inflation doesn’t eat it alive.

Measure more than net worth

Net worth is useful, but it’s not the whole story. Consider three dashboards:

- Liquidity: How long could you cover essentials if income stops?

- Stability: Are your monthly obligations manageable, or are they one rate hike away from chaos?

- Future security: Are you building assets that can support you later (retirement, home equity, investments)?

A household might have modest net worth but strong cash flow and low debtmeaning less stress. Another might have higher net worth but be

house-rich and cash-poormeaning stress with better decor.

So… Is the Median Net Worth “Alarmingly Low”?

If you define “alarming” as “most households are one shock away from financial pain,” then yesthe median can feel alarmingly low, because it doesn’t

guarantee resilience. It’s a middle number in a country with steep inequality, high housing costs, rising debt balances, and a cost of living

that keeps finding new ways to surprise you.

The median also acts like an economic warning light. When the typical household’s wealth is heavily tied to housing, when liquid savings are thin,

and when debt balances keep rising, it suggests the financial system is stable for some and stressful for many. That’s not just a personal finance issue;

it’s a societal onebecause a nation of anxious households doesn’t exactly radiate “healthy economy” energy.

The good news (yes, there’s good news) is that wealth is not a personality trait. It’s often the result of time, access, and compounding. The better news

is that when households gain access to stable income, affordable credit, and asset-building opportunities, median wealth can rise. The goal isn’t to make

everyone a millionaire overnight. It’s to make “a small emergency” feel small again.

Experiences That Make the Median Net Worth Feel Low (Real-Life Snapshots)

Numbers are helpful, but experiences are what make the situation feel real. Here are common, realistic snapshots of how “low median net worth” shows up

in everyday American lifewithout assuming anyone is irresponsible or making cartoonish choices.

1) The renter who’s doing everything rightand still can’t get traction

This household pays rent on time, avoids flashy spending, and even manages to save a little. But rent increases arrive like an annual tradition,

and moving is expensiveapplication fees, deposits, furniture that doesn’t fit, time off work. Their net worth grows slowly because they’re not building

home equity, and their savings often get redirected into “life happens” costs. They’re not failing; they’re simply living in a system where the main

middle-class wealth engine (homeownership) is harder to access.

2) The new homeowner who’s “wealthy” on paper but feels broke in practice

This household finally buys a home. Their net worth jumps because they now have equity. But month-to-month, they’re stretched: mortgage payment, insurance,

repairs, and the delightful surprise of “your water heater has retired.” They may have a higher net worth than before, yet their emergency fund is thin

because so much cash is tied up in the house. The wealth is realbut it’s not always usable when the car needs new tires today.

3) The debt juggling act that quietly reshapes the future

Another household has student loans, a car payment, and a credit card balance that started as “temporary.” They work steadily, but high interest costs

make it hard to build savings. They’re not buying luxury vacations; they’re paying for normal life while borrowing gets more expensive. Over time, this

can turn into a wealth gap: households with cheaper access to credit can invest and build assets, while households paying higher interest are stuck paying

for yesterday.

4) The caregiver household where time is the scarce resource

Care responsibilitieskids, aging parents, family members with disabilitiescan limit work hours, reduce job flexibility, and increase expenses.

This household might earn enough to cover basics, but saving and investing become inconsistent. Their “wealth plan” gets interrupted by real obligations:

medical co-pays, transportation, childcare gaps, missed promotions. The experience isn’t just financial; it’s emotionalbecause the household is spending

energy on keeping everyone afloat, not on building assets.

5) The “middle” household that looks stable until one shock hits

Plenty of households sit near the median with a decent net worth number, yet rely on steady income to keep everything balanced. Then a shock hits:

a layoff, reduced hours, a health issue, a divorce, or even a major repair. Without a large liquid buffer, the household turns to debt or drains retirement

savings. Net worth can fall quicklyand the recovery can take years. This is why the median feels alarming: not because the middle is “nothing,” but because

the middle can be fragile.

These experiences are common because wealth is often less about budgeting trivia and more about big structural forces: housing costs, debt terms, benefits,

income stability, and access to appreciating assets. When the median net worth sits around a number that sounds “fine,” but many households still struggle

with emergencies, it tells us the economy is producing wealthbut not consistently producing financial breathing room.