Table of Contents >> Show >> Hide

- What Life Expectancy Really Means (and What It Doesn’t)

- What Is Longevity Risk?

- Why Planning Around the “Average” Can Backfire

- The Sneaky Sidekick: Sequence of Returns Risk

- Common-Sense Ways to Manage Longevity Risk

- A Wealth of Common-Sense Rules for Longer Lives

- Real-World Experiences – And What They Teach Us

If you’ve ever plugged your age into a life expectancy calculator and thought,

“Great, I just have to make my money last until that age,” I have some

slightly uncomfortable news: that’s not how this works.

Life expectancy is an average, not an expiration date. Some people, sadly,

don’t make it to traditional retirement age. Others happily blow past 90,

collecting birthday cards and Social Security checks like it’s a hobby.

Somewhere in the middle sits your retirement plan, nervously wondering how

long it has to last.

That uncertainty is what the finance world calls longevity risk:

the risk that you live longer than your money does. It sounds like a good

problem to havewho doesn’t want more years?until you’re staring down rising

costs, market volatility, and a portfolio that’s shrinking faster than your

patience.

The good news: you don’t need a PhD in actuarial science to manage longevity

risk. You just need a bit of data, a bit of humility, and a decent amount of

common sense. Let’s break it down.

What Life Expectancy Really Means (and What It Doesn’t)

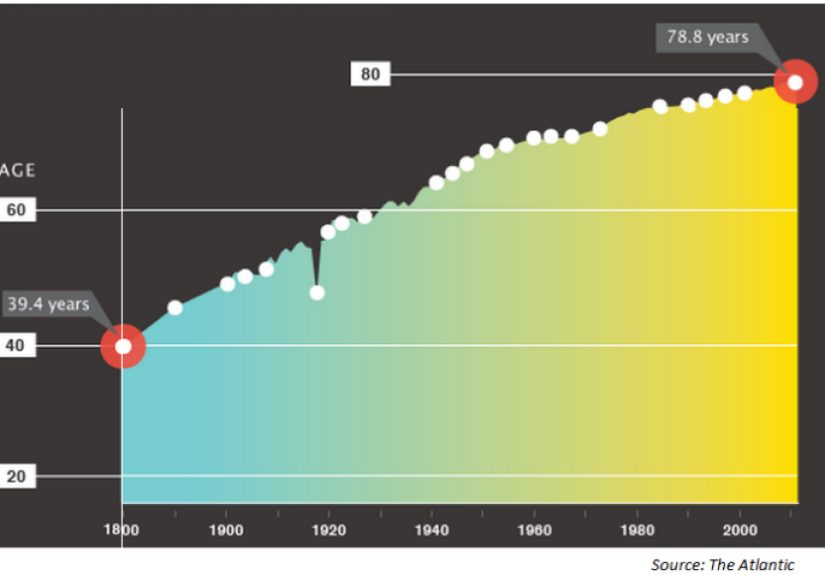

When headlines say “U.S. life expectancy is about 78 years,” that’s a population

average, influenced by infant deaths, accidents, chronic disease, and a lot of

messy real-world factors. It’s not telling you personally when you’re

likely to dieit’s telling you roughly how a very large group of people has

fared.

More relevant for retirement is something called remaining life expectancy.

For example, if you make it to age 65, your average remaining years are

longer than the birth-average suggests, because you’ve already survived the

earlier riskier decades. Social Security life tables show that a 65-year-old

American can easily have 18–20+ years ahead on average, with a meaningful

share living into their late 80s and 90s.

There’s another catch: averages hide the spread. If the “average” 65-year-old

man lives to 84, that doesn’t mean most men die at 84. It means some die in

their 70s, some in their 90s, and a few seem determined to outlive their

investment advisor.

Why Your Personal Life Expectancy May Be Higher

For many people who are actively planning retirementespecially those with

higher education, better access to healthcare, and healthier lifestyles

personal life expectancy is often higher than the national average.

That’s great news for your future self, but bad news for any retirement plan

built on a conservative “I’ll probably be gone by 80” assumption.

This is why many planners suggest modeling your financial plan out to age 90,

95, or even 100. You may not make it therebut if you do, you’ll be very glad

you planned for the “long life” scenario instead of the “average life” fantasy.

What Is Longevity Risk?

Longevity risk is the financial risk that you outlive your

assets. It shows up in a few different ways:

- For individuals: the risk that your savings, investments,

and pensions don’t stretch as far as your lifespan. - For pensions and insurers: the risk that people live longer

than expected, forcing them to pay out more benefits than they priced in. - For governments: the pressure on Social Security, Medicare,

and public finances as large populations live longer and need support longer.

Longer lives are a huge social win. But financially, they transform a

10–15-year retirement into a possible 25–35-year span. That’s not just

“extra vacation.” That’s decades of housing, food, healthcare,

and inflation that your money has to keep up with.

The Slow Creep of Longer Lives

Improvements in medical care, public health, and lifestyle have nudged life

expectancy upward over time. The increases may look modestfractions of a year

per decade at older agesbut even a few extra years across millions of retirees

adds up to serious additional cost.

For your personal plan, that “modest” improvement can mean needing to fund

three, five, or ten more years of retirement than your parents did.

Underestimating that is like planning a road trip and forgetting the last

200 miles still need gas money.

Why Planning Around the “Average” Can Backfire

One of the most common mistakes people make is mentally anchoring to an

average life expectancy and building their retirement plan around it. Something like:

“My calculator says 84. I’ll plan money until 84.”

The problem is simple: you only get to retire once.

If you underestimate and live longer than planned, you can’t go back and say,

“My bad, I’d like to redo the saving part.”

Research consistently finds that people underestimate how long they might live

and how many years they’ll spend in retirement. At the same time, we’re seeing

disturbing trends in premature deaths among some groups. In other words,

longevity risk isn’t evenly spread. It’s shaped by health, income, race,

geography, and lifestyle.

That makes the averages even less helpful. For a relatively healthy

middle-class non-smoker nearing retirement, it’s often more realisticand safer

to assume a longer horizon than the country-level statistics would suggest.

The Asymmetry Problem

Here’s the key: the downside of overestimating your lifespan is mild

(you die with extra money and your heirs think you’re a genius). The downside

of underestimating is brutal (you’re alive, but your portfolio is not).

That asymmetry alone justifies planning for the long end of the range. When

in doubt, give your future self more runway, not less.

The Sneaky Sidekick: Sequence of Returns Risk

Longevity risk rarely travels alone. It usually brings a friend:

sequence of returns risk.

Sequence of returns risk is what happens when you retire into

bad timingmarket downturns early in retirementwhile you’re also

withdrawing from your portfolio. Your average return over 30 years might look

perfectly fine on paper, but if the first five years are ugly and you’re

pulling money out the whole time, your portfolio may never fully recover.

Think of two retirees with identical portfolios and identical average returns:

- Retiree A gets strong returns early and weak returns later.

- Retiree B gets weak returns early and strong returns later.

Their long-term averages match, but their outcomes don’t. Retiree B may run

out of money years earlier because they had to sell assets at depressed prices

in those early bad years. Once that damage is done, even great returns later

can’t fully fix itbecause there’s less money left to grow.

Combine that with longevity risk and you have a dangerous combo:

living longer, but starting retirement with a wounded portfolio.

That’s why sequence of returns risk deserves a seat at the planning table

alongside life expectancy.

Common-Sense Ways to Manage Longevity Risk

You can’t control how long you live or what the stock market does next year.

But you can stack the odds in your favor with a few practical moves.

1. Plan for a Long Life, Not an Average One

When running projections, don’t stop at 85. Ask:

“What if I live to 92? 95? What if one spouse lives much longer than the other?”

Many planners now default to at least age 90–95 for one spouse in a couple.

That doesn’t mean you’ll definitely make it there, but if you do, your

retirement plan won’t be gasping for air in your late 80s.

2. Save More Than Feels Comfortable

This one isn’t fun, but it’s powerful. Longer life expectancy means more years

of expenses, and that usually means higher savings targets.

Health-based longevity research shows that additional years of life translate

into a substantial increase in the total capital needed to maintain your

standard of living.

If you’re behind, don’t panicbut also don’t assume you can fix everything

with clever investing. Higher savings rates and longer working years often do

more heavy lifting than chasing yield.

3. Be Smart About Social Security Timing

Social Security is one of the best inflation-adjusted longevity hedges you have.

The longer you wait to claim (up to age 70), the higher your monthly benefit.

For people with average or better health and sufficient savings to bridge the

gap, delaying benefits can be a powerful way to insure against a

long life.

It’s not the right move for everyonehealth, marital status, and income all

matterbut think of claiming decisions as a longevity risk lever, not just a

race to “get your money back.”

4. Diversify Like Your Future Depends on It (Because It Does)

Many retirees instinctively pile into cash and bonds because they feel “safe.”

The problem is that over 20–30 years, inflation can quietly hollow out those

“safe” assets. Studies of retiree portfolios show that over-allocating to

conservative assets may feel comforting in the short run but increases the risk

of running out of money in the long run.

A more resilient approach blends:

- Equities (for long-term growth and inflation protection),

- Bonds and cash (for stability and near-term spending),

- Possibly other assets like real estate or inflation-linked bonds.

The key is matching your time horizon. Money you won’t touch

for 15–25 years is playing a different game than the cash you need next year.

5. Think About Longevity Insurance (a.k.a. Annuities)

Annuities get mixed press, sometimes deservedly, but at their core they’re

simply a way to transfer longevity risk to an insurer. In

exchange for a lump sum, you receive a guaranteed income stream for life.

There are many flavorsimmediate annuities, deferred income annuities,

fixed indexed annuities, and more. Not all are created equal, and fees and

complexity can be a problem. But when structured well, using a slice of your

portfolio to buy lifetime income can:

- Reduce the pressure on your remaining investments,

- Provide psychological comfort (“the paycheck never stops”),

- Directly hedge the risk of hitting age 95 with too little left.

Think of these products as “pensions you buy for yourself,” not magic

investments. They’re a risk-transfer tool, not a growth engine.

6. Work Longer or Differently

One of the most underrated longevity strategies is simply

earning income longer. Even a few extra working years can:

- Shorten the number of years your portfolio must support you,

- Allow you to save more at the tail end of your career,

- Delay Social Security and retirement account withdrawals.

Increasingly, many Americans continue working into their 70s and even 80s,

sometimes out of necessity and sometimes because work provides meaning,

structure, and social connection. If your health and job allow it, think

about a phased retirement, part-time consulting, or a “second-act” career

that blends income and enjoyment.

A Wealth of Common-Sense Rules for Longer Lives

If you strip away all the jargon, longevity planning comes down to a handful

of common-sense principles:

- Assume you’ll live longer than you think. Your healthy

future self will thank you. - Avoid all-or-nothing bets. Don’t be 100% in cash or

100% in risky stocks; build a flexible, diversified mix. - Protect the early years of retirement. Sequence of

returns risk is highest when you first start drawing down. - Turn some assets into dependable income. Pensions,

Social Security, and annuities can be powerful stress reducers. - Keep your plan updated. Health changes, markets move,

goals evolve. Your retirement plan should be a living document, not a

one-time spreadsheet you stash in a drawer.

The goal isn’t to predict the exact year you’ll die. The goal is to create

a financial life that works well across a wide range of outcomeseven the

pleasantly surprising ones.

Real-World Experiences – And What They Teach Us

Theory is nice, but longevity risk becomes very real when you look at

actual lives. Here are a few composite “characters” that reflect common

patterns financial planners see. If any of them sound familiar, that’s

your cue to update your own plan.

Olivia, the Overconfident Optimist

Olivia retired at 62 because she was “done with work.” She used an online

calculator that told her she’d likely live to 83. So she planned for

20 years of retirement, set a generous withdrawal rate, and bought a

vacation condo to celebrate her newfound freedom.

The first few years were greatmarkets were strong, her portfolio looked

healthy, and she started to think she’d over-saved. Then the market turned,

just as inflation picked up and property costs rose. Suddenly, her

withdrawals were coming out of a shrinking pool of assets.

At 75, she’s still healthy, but the math is getting uncomfortable.

She’s now considering selling the condo and cutting back on discretionary

spending to make her money last if she lives into her 90s. She isn’t

doomed, but she wishes she’d planned for 30 years instead of 20 from

the beginning.

Lesson: Don’t anchor your plan to a “most likely” life span.

Plan for a plausible long life in advance, so you’re not scrambling later.

Dan, the Data-Driven Planner

Dan is the kind of person who loves spreadsheets almost as much as coffee.

In his mid-50s, he started researching life expectancy by age, health, and

family history. He realized that there was a very real chance he or his

spouse could live into their early 90sor beyond.

Instead of panicking, Dan used this information to tweak his plan:

- He increased his savings rate for his final decade of work.

- He decided to delay Social Security to boost those

inflation-adjusted payments. - He took part of his retirement assets and bought a simple,

low-cost income annuity that starts paying at age 80, creating

a safety net if he lives very long.

When he finally retired, he didn’t feel bulletproofbut he did feel that his

plan would hold up under a lot of different futures. That sense of confidence

is one of the most underrated “returns” good planning delivers.

Lesson: You can’t predict the future, but you can design a

plan that’s hard to break.

Lina, the Late Bloomer

Lina didn’t start saving seriously until her late 40s. Life, kids, and

career changes kept getting in the way. When she finally sat down with a

planner at 55, the numbers were… sobering.

Instead of giving up, Lina reframed the problem. She decided that her

“full retirement” might not happen at 62 or even 65. She aimed for a

phased retirement:

- Full-time work until 67,

- Then part-time consulting into her early 70s,

- Gradually stepping down only when she felt secure.

By extending her earning years and keeping some income flowing, she reduced

the number of years her portfolio had to fund entirely on its own. She also

stayed socially and mentally engaged, which didn’t hurt.

Lesson: If you’re starting late, your most powerful levers

may be working longer and spending smarter, not chasing aggressive

investments.

The Lees, the Multi-Generational Planners

The Lees watched their parents run out of savings in their late 80s and

decided they wanted a different outcome. In their 50s, they had a family

meeting with their adult kidsnot to demand support, but to be transparent.

They shared:

- How long their own parents had lived,

- What their current retirement savings looked like,

- How they were planning for healthcare and long-term care,

- What they hoped to leave (or not leave) as an inheritance.

This openness led to better decisions all around. The Lees felt freer to

purchase an annuity and consider long-term care coverage, knowing their kids

understood the trade-offs. Their children, in turn, started their own

retirement saving earlier, having seen firsthand how longevity can strain

finances.

Lesson: Longevity risk isn’t just an individual issueit’s

a family story. Talking about it early can reduce stress later.

Bringing It All Together

Longevity risk is not about being morbid. It’s about being realisticand kind

to your future self. You don’t need perfect forecasts. You just need a plan

that:

- Assumes a reasonably long life,

- Builds in buffers for bad market timing,

- Uses tools like Social Security, diversification, and annuities wisely,

- Stays flexible as your life, health, and goals evolve.

That’s not doom and gloom. That’s a wealth of common sense. The goal isn’t

to die with zero dollars on the exact right day. The goal is to live your

longest life with the freedom, dignity, and options that good planning can

buy.