Table of Contents >> Show >> Hide

- Where the “33% slowdown” came from

- Why growth slowed so sharply in Q1

- What the slowdown looked like in the numbers

- Why Q1 can feel especially rough

- What “33% harder” actually meant inside a SaaS company

- Who handled the slowdown best

- How founders and growth teams adapted

- Experiences from operators who lived through the slowdown

- Conclusion

- SEO Metadata

There are business headlines that whisper, and then there are business headlines that walk into the room, kick over a chair, and announce that the easy-money era is over. “Growth Slowed Down About 33% On Average For Everyone in Q1” is very much in the second category.

In the SaaS and cloud software world, that line became shorthand for a brutal reality: the market did not stop buying software, but it definitely stopped buying it with the carefree enthusiasm of the boom years. Budgets tightened. Sales cycles stretched. Expansion revenue got pickier. New logos became harder to win. Suddenly, growth did not disappear, but it did start wearing ankle weights.

That is what made the “about 33%” figure so sticky. It was not saying every company fell apart. It was saying the game got harder for almost everybody at the same time. And if you felt like your pipeline had lost some pep, your demo-to-close rate had become moody, or your once-happy upsell motion had started ghosting you, congratulations: you were not uniquely cursed. You were living through a broad market reset.

This article unpacks where that slowdown came from, why it hit so many SaaS companies at once, what the numbers really mean, and what founders, marketers, operators, and revenue teams can learn from it now. Because while the pain was real, the lesson is not “growth is dead.” The lesson is much more useful: durable growth is harder, cleaner, and a lot less impressed by hype than it used to be.

Where the “33% slowdown” came from

The phrase itself comes from SaaS commentary that pulled together two different sets of evidence pointing in the same direction. One dataset focused on private SaaS startups, and another looked at top public SaaS and cloud companies. Different samples, same headache.

On the private-company side, benchmark data showed that SaaS growth had come down materially from the fever-dream highs of 2021. On the public-company side, net new bookings and broader expansion signals were also meaningfully weaker. Put simply, both private and public software businesses were telling versions of the same story: growth was still happening, but it was happening with less momentum, more friction, and a lot more executive sweating.

That is important because it ruled out the comforting explanation that “it’s just us.” When two different slices of the software market show similar deceleration, you are no longer looking at a one-off sales problem. You are looking at a market-wide change in buying behavior.

And that change was not tiny. A one-third slowdown is not a rounding error. It is the difference between a company that looks like a breakout rocket and one that suddenly needs a very serious board slide called “efficiency initiatives.”

Why growth slowed so sharply in Q1

1. Buyers went from curious to cautious

During the fast-growth software cycle, many teams bought tools because they wanted to move faster, experiment more, and avoid falling behind. In the slowdown cycle, the question changed. Instead of asking, “Could this help?” buyers asked, “Can you prove this pays for itself by Tuesday?”

That shift sounds subtle, but in practice it changes everything. Nice-to-have products get stuck in evaluation limbo. Mid-funnel enthusiasm cools off. Pilots expand more slowly. Procurement suddenly becomes the star of the show, which is about as exciting as finding out your vacation now includes a mandatory tax seminar.

2. New logo acquisition became harder

For many SaaS companies, new customer acquisition was the first place the slowdown showed up. Even when demand still existed, it became harder to convert interest into actual contracts. Committees got larger. CFO sign-off showed up earlier. Smaller customers delayed decisions. Larger customers pushed for better terms.

That meant revenue teams had to work harder for the same outcome. More meetings were needed to close the same deal. More follow-up was needed to keep momentum alive. More proof was required to overcome the universal buyer objection of the era: “We like this, but let’s revisit next quarter.”

3. Retention stayed good, but not as magical

SaaS leaders love recurring revenue because it makes the business model look sturdy, elegant, and almost suspiciously attractive in investor decks. But during the slowdown, retention stopped being a free tailwind.

Customers did not necessarily churn in huge numbers, but many did optimize seats, reduce usage, consolidate vendors, or delay expansion. That matters because high-growth SaaS companies often rely on existing customers to do more of the heavy lifting over time. When expansion revenue softens, total growth slows even if the product is still valuable and logos are still sticky.

In other words, the slowdown was not always caused by customers leaving. Often, it came from customers staying… but spending more carefully. That is less dramatic than churn, but financially it still stings.

4. Public market pressure changed private-company behavior

Once public SaaS valuations reset, everyone started acting differently. Founders adjusted hiring plans. Boards pushed harder on burn. Investors asked for efficiency, not just top-line swagger. Go-to-market leaders were told to deliver growth, yes, but preferably without setting money on fire like a confused wizard.

That matters because software companies do not operate in a vacuum. If public comps fall, private expectations change. If valuation multiples compress, tolerance for sloppy growth shrinks. So even companies that still had demand had to operate differently. The market was saying, loud and clear: “Congratulations on your growth. Now please explain how expensive it is.”

What the slowdown looked like in the numbers

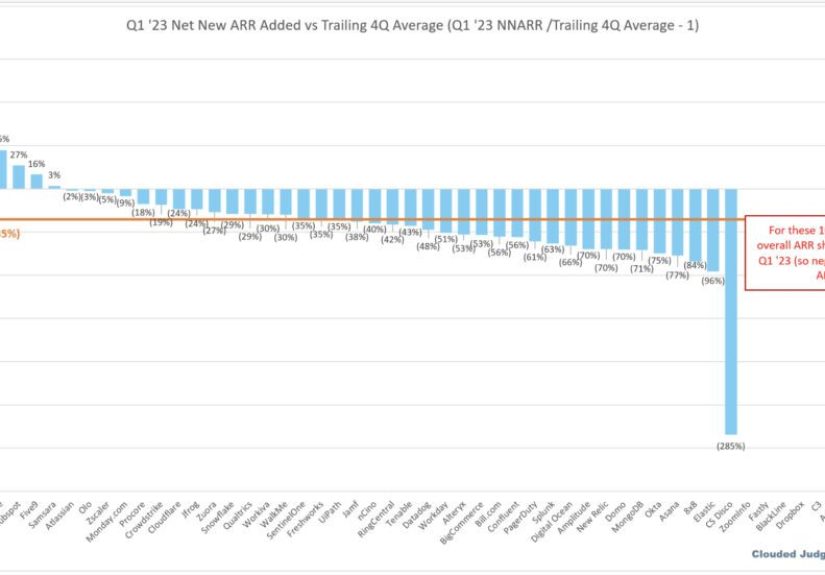

The data behind the headline is messy in the way real business data always is, but the pattern is consistent. Private SaaS benchmarks showed that top growth rates were still well below their earlier highs. Public cloud analysis later showed that aggregate net new ARR could still slump by nearly 30% year over year in a tough quarter, which tells us the aftershocks of the slowdown did not vanish overnight.

At the same time, the broader software market never fully collapsed. Software spending forecasts continued to rise, cloud leaders remained enormous, and the best companies still found ways to grow quickly. That creates a useful nuance: the slowdown was real, but it was not universal doom. It was selective pressure.

That distinction matters. If overall software budgets still grow while individual vendors struggle, the problem is not simply “nobody is spending.” The problem is “buyers are concentrating spend on the tools that feel essential, fast to value, and hard to replace.”

That is why some companies slowed dramatically while others kept moving. A broadly tougher market does not eliminate winners. It just makes winning less casual.

Why Q1 can feel especially rough

Quarter one has a strange personality. In theory, it can be a reset quarter full of fresh budgets and clean planning cycles. In practice, it can also be the quarter where companies confront reality.

Leadership teams review the prior year, tighten priorities, cut experiments, and ask every department to defend spend. Sales organizations walk into the year with targets that still smell faintly of optimism, only to discover that customers have begun the year in a deeply non-optimistic mood. Marketing teams that hoped for a quick rebound learn that traffic is not the same as intent. Customer success teams discover that renewal conversations now include phrases like “consolidation strategy” and “tool rationalization,” which are corporate synonyms for “please prepare to be judged.”

That is why a slowdown in Q1 can feel worse than the raw number suggests. It is not just a weaker quarter. It is a weaker quarter arriving right when everyone wanted a fresh start.

What “33% harder” actually meant inside a SaaS company

When operators say the market got 33% harder, they usually do not mean exactly one-third fewer opportunities magically appeared. They mean everything became incrementally more difficult at once.

Pipeline quality got wobblier. Close dates slipped. Multi-product deals got split into smaller purchases. Champions needed more internal support. Free trials took longer to convert. Expansion conversations became budget-defense exercises. Forecasts looked fine until the final week, and then suddenly everyone developed a close plan and a facial twitch.

In that environment, old growth playbooks started breaking down. You could not just spend more on acquisition and expect efficient output. You could not assume product usage would naturally expand into bigger contracts. You could not assume hiring more reps would manufacture demand. In many cases, teams had to relearn the fundamentals: sharper positioning, tighter qualification, faster time-to-value, stronger onboarding, and more ruthless focus on ideal customers.

This was not glamorous work. Nobody throws a parade for “reduced payback period by three months.” But that kind of discipline became the difference between a company that merely survived the slowdown and one that emerged stronger from it.

Who handled the slowdown best

The companies that held up best usually had one or more of the following traits: clear ROI, mission-critical use cases, strong retention, low-friction expansion, or products tied to areas where buyers were still willing to spend aggressively.

That last category has increasingly included AI-related software, infrastructure, and workflow tools. Recent cloud benchmarks show that AI-heavy businesses have helped pull average growth rates back upward in parts of the market. That does not mean slapping “AI-powered” on a landing page suddenly fixes everything. Buyers are too sharp for that. It does mean that when a product clearly saves time, automates work, or increases output in a measurable way, budgets suddenly become more cooperative.

The lesson is not that every SaaS company must become an AI company. The lesson is that the market rewards products that feel urgent, not just interesting. Urgency is the new growth lubricant.

How founders and growth teams adapted

1. They narrowed the ideal customer profile

Instead of chasing every lead with a pulse and a corporate email address, smart teams got stricter about who they sold to. The goal was not more meetings. It was more meetings with buyers who had pain, budget, and a decent reason to move this quarter.

2. They moved closer to measurable ROI

Messaging changed from “transform your workflow” to “reduce costs, save time, increase output, and here is the proof.” Vague promise language lost power. Specific business outcomes gained it.

3. They obsessed over retention and expansion

When new logo growth gets harder, the installed base matters more. That pushed customer success, onboarding, and product adoption much closer to the center of the growth strategy. Companies stopped treating retention like a housekeeping metric and started treating it like the main character.

4. They accepted that efficient growth beats theatrical growth

The old badge of honor was “grow at all costs.” The newer badge became “grow well enough that no one panics when you show the margin slide.” It is less sexy, but much better for sleeping.

Experiences from operators who lived through the slowdown

If you talk to founders, CROs, marketers, and customer success leaders who went through this period, the stories start sounding eerily similar. Not identical, but close enough that you begin to suspect the whole software industry was trapped in the same group project.

One founder would say the pipeline still looked healthy at first glance, but when the team dug in, they found buyers moving more slowly, asking more finance-related questions, and breaking one large rollout into three smaller decisions. Another operator would explain that demos were still being booked, yet the emotional temperature of those calls had changed. Buyers were less excited by possibility and more interested in proof, implementation burden, and how quickly the tool could produce an obvious win.

Marketing teams felt it too. Traffic might still arrive. Content might still perform. Events might still generate leads. But a lead stopped meaning what it used to mean. It was no longer enough to create attention. Teams had to create confidence. Campaigns that once worked because they were clever now had to work because they were useful, concrete, and painfully specific about business value.

Sales leaders often describe the slowdown as death by a thousand tiny delays. It was not always a dramatic no. Often it was, “This is great, but legal needs another review.” Or, “We’re interested, but let’s start with one team instead of six.” Or the classic corporate breakup line: “Can you circle back in a quarter?” In many organizations, forecasting became less like math and more like weather prediction with nicer dashboards.

Customer success teams had their own version of the experience. They found that even happy customers had changed. Customers still liked the product, but they were now under pressure to justify every vendor in the stack. That meant CSMs needed stronger adoption plans, stronger executive relationships, and stronger renewal narratives. “They love us” was no longer enough. The question became, “Can they defend us in a budget meeting?”

Finance teams, unsurprisingly, had the time of their lives. Suddenly everyone cared about CAC payback, gross margin, expansion quality, burn multiple, and whether growth was real or just expensive. Plenty of operators learned a useful lesson in this phase: discipline is annoying right up until the moment it saves you.

And yet, hidden inside the stress was something healthy. Teams got sharper. Messaging improved. Bad-fit customers became easier to spot. Product leaders focused harder on features that delivered visible value. Revenue leaders stopped confusing activity with progress. In a strange way, the slowdown forced SaaS companies to become better businesses.

That is why so many operators look back on the period with a mix of exhaustion and respect. It was not fun. It was not cute. But it did separate durable companies from companies that had been surfing a market wave and calling it genius.

Conclusion

“Growth Slowed Down About 33% On Average For Everyone in Q1” landed because it captured a real mood shift in SaaS: growth did not vanish, but it became materially harder to earn. Budgets tightened, buyers got tougher, retention lost some shine, and the market started rewarding efficiency almost as much as expansion.

That may sound discouraging, but there is a useful upside. When a market gets harder, weak habits get exposed fast. The companies that win are the ones with sharper positioning, faster time-to-value, healthier retention, stronger discipline, and products customers can actually justify buying.

So yes, the quarter felt worse. Yes, the slowdown was real. But it also clarified what sustainable SaaS growth looks like. Less sugar rush, more muscle. Less fantasy, more fit. And honestly, that is not a bad trade if you are trying to build something that lasts longer than the next shiny cycle.